The Benefit of Discretion: Active Versus Passive Management for Institutional Investment-Grade Fixed Income

June X, 2026

The active-versus-passive debate in institutional investment-grade (IG) fixed income too often focuses exclusively on fees. While passive management can offer low-cost, low-tracking-error market exposure and may be appropriate in certain fixed income allocations, these strategies are built to follow benchmark rules rather than make independent valuation judgments security by security. This can leave investors holding securities because they remain in the index even if valuations or fundamentals are no longer compelling.

This is particularly true in institutional IG fixed income where structural considerations like benchmark construction, index eligibility, issuer heterogeneity, and uneven liquidity can make rules-driven strategies especially limiting and active management especially relevant. Rules-based approaches may also limit a manager’s ability to mitigate credit risk if an issuer’s creditworthiness is deteriorating but remains in the index. Collectively, these features create opportunities for skilled active managers to add value and manage risk more effectively than a purely passive, rules-based approach.

The Nature of Institutional IG Fixed Income

IG fixed income markets consist of thousands of heterogeneous securities across numerous sectors with varying structures, liquidity, and contractual features. Fixed income investing requires not only a view on issuer fundamentals, but also expertise in security structure, relative value analysis, liquidity assessment, yield curve positioning, and portfolio construction.

These nuances matter when the objective is more complex than tracking an index. Institutional portfolios are often also managed against duration targets, credit quality limits, liquidity needs, income requirements, capital charges, tax considerations, accounting effects, and downside risk. That multidimensional mandate favors an active approach.

Passive Strategies Are Rules-Driven

Passive management seeks to replicate the risk and return characteristics of a benchmark index, whether through full replication, stratified sampling, or optimization. Its appeal is straightforward: low fees, transparency, diversification, minimal tracking error, and reduced manager selection risk. These strategies are generally beholden to index rules and, therefore, face several limitations.

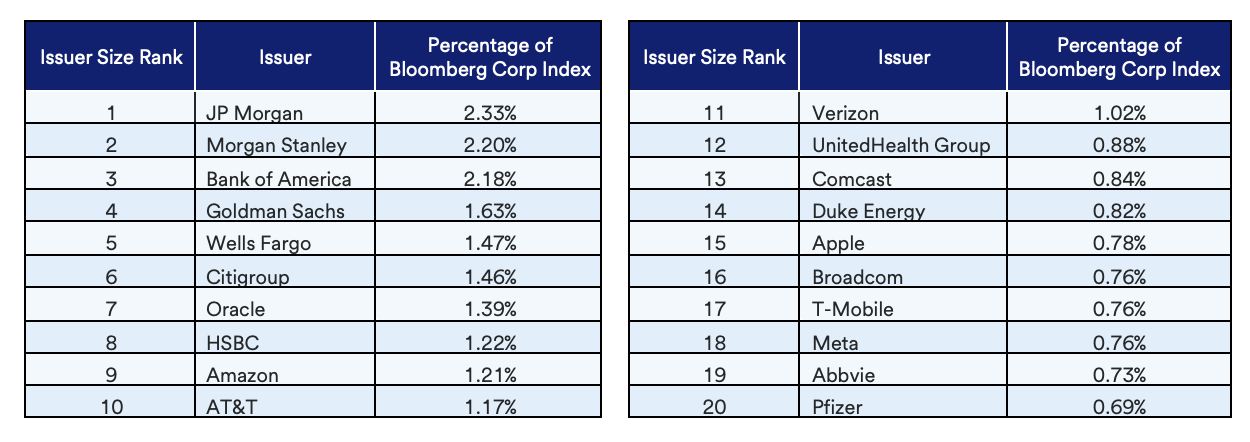

First, most bond indices are market-value weighted, so issuers with the most debt outstanding receive the largest weights. Debt-weighted indexing allocates more capital to entities that have borrowed the most without regard to compensation for risk. This makes allocation decisions a rules-driven outcome rather than a valuation-led credit judgement.

As of May 29, 2026, seven of the eight largest issuers in the corporate bond component of the Bloomberg U.S. Aggregate Bond Index were banks, while the largest non-financial corporate issuer was Oracle.

Passive strategies are also constrained by index turnover and forced trading as bond indices regularly add and remove securities which no longer meet index eligibility requirements for various reasons. Passive managers must respond to these changes, which can create transaction costs and limit manager discretion regarding trade execution.

The decision framework for passive portfolios is also less flexible because it is designed to mirror benchmarks, not to add value by avoiding deteriorating credits, adjusting to changing liquidity conditions, or exploiting relative value dislocations. Most fixed income indices also rebalance once monthly and generally cannot capture new-issue credit spread concessions available on bonds issued intra-month.

Finally, IG fixed income indices often contain thousands of securities, many of which are illiquid or unavailable in the desired size. Passive managers therefore often rely on sampling rather than full replication, introducing tracking error, liquidity differences, and unintentional factor exposures.

Active Management Uses Deliberate Decision-Making

The practical limitation of rules-driven investing occurs when benchmark exposure diverges from what valuation, downside protection, liquidity conditions, or portfolio objectives would otherwise suggest.

Active management tools are based on discretion: credit and issuer selection, sector allocation, yield curve positioning, duration management, security structure, liquidity management, and relative value trading. These decisions are made independent of any given security’s inclusion in the benchmark, allowing managers to make decisions based upon relative value and risk management.

Credit and issuer selection are important sources of potential value, particularly because issuers vary materially in risk, including those within the same rating category or industry. Active managers can overweight improving credits, avoid deteriorating issuers, and seek bonds whose spreads adequately compensate for underlying risk. They can also invest beyond the benchmark’s eligible universe, including privately placed Rule 144A securities which may be excluded from the index solely due to the issuance structure even when issued by companies whose publicly traded bonds are included in the index. Active managers therefore may have access to a broader opportunity set across corporate and securitized markets.

Active managers can also adjust allocations across corporate bonds, Treasuries, agencies, securitized debt, and other sectors whose performance varies across economic regimes. This flexibility to change allocations depending on valuations and macroeconomic conditions can be valuable when actively managing around inflection points in the business and economic cycle.1

From a duration and curve perspective, passive portfolios inherit the underlying characteristics of the benchmark. Active managers can adjust positioning based on monetary policy, inflation expectations, and relative value across maturities. Even modest deviations from the benchmark can meaningfully affect performance and risk.

Active managers can also evaluate differences in security structure between bonds that appear similar on the surface yet differ meaningfully in economic terms. A passive index may treat securities as eligible based primarily on index rules and may be forced to ignore this important source of both expected return and downside risk.

They can also benefit from implementation and trading opportunities passive strategies typically cannot capture. These include:

- Rolling agency mortgage-backed securities when dollar rolls are trading special

- Stacking front-end yield given attractive break-evens over a 1-year investment horizon

- Capturing new issue spread concessions

- Swapping between mispriced securities within the same issuer

- Trading strategies aimed at capturing value from amortizing asset-backed securities that migrate higher in credit quality over time as the underlying assets amortize

Active managers may also benefit from inefficiencies created by passive and rules-based investors. When passive funds must trade because of month-end rebalancing, maturity roll-down, rating migration, or issuance patterns, active managers may be able to act opportunistically.

Lastly, active managers can mitigate the risk of becoming forced sellers by maintaining liquidity buffers, avoid crowded index trades, and position portfolios to meet cash flow needs. To contrast, passive managers may be required to do so if a security falls out of the index. This is particularly important in stressed markets when bid-ask spreads can widen materially and trading conditions can deteriorate quickly.

Discretion Can Limit Downside Risks

Discretion matters most when institutional portfolios require more than simply trying to reproduce the benchmark. This is particularly important in managing downside risk, avoiding deteriorating credits, and aligning portfolios with specific liabilities or constraints.

In fixed income, avoiding losses and managing downside risk can be as important as identifying winners. Upside is generally limited to coupon income and spread tightening, while the downside from downgrades, credit events, liquidity shocks, or spread widening can be substantial. Active managers can seek to avoid issuers whose fundamentals are deteriorating before it is fully reflected in index membership or market pricing.

This is particularly relevant for BBB-rated securities, which represent a meaningful portion of many investment grade credit indices. Whereas a passive investor must generally hold BBB exposure according to benchmark weight, an active manager can choose to overweight stable BBB credits and underweight those at risk of being downgraded to high yield. This can preserve capital and reduce forced-selling risk.

Active management is also better suited to institutions with specific objectives, liabilities, and constraints instead of generic benchmark exposure. Insurance companies may prioritize capital efficiency, book yield, and regulatory treatment. Pension plans may focus on liability matching and funded-status volatility. Endowments and foundations may emphasize liquidity and diversification. Corporate treasury portfolios may focus on principal stability and cash flow certainty. Active managers can design portfolios around those objectives in ways passive index products cannot.

Cost Considerations

The most common argument for passive management is cost. Institutional investors are right to scrutinize fees and expect active managers to justify them through repeatable alpha generation and meaningful portfolio customization.

However, in IG fixed income, headline management fees are only one part of the economic equation. Transaction costs, market impact, liquidity costs, downgrade avoidance, tax considerations, and risk-adjusted performance also matter. A low-fee passive strategy may be less attractive if it forces exposure to unattractive issuers, inherits poor benchmark construction, or underperforms during periods of market stress.

As such, the more important comparison is whether an active manager can deliver better net-of-fee outcomes after accounting for risk, liquidity, customization, and downside protection. This means the more relevant question for institutional investors is whether active managers, in aggregate and net of fees, have added enough value to justify the additional cost.

Performance Measurement

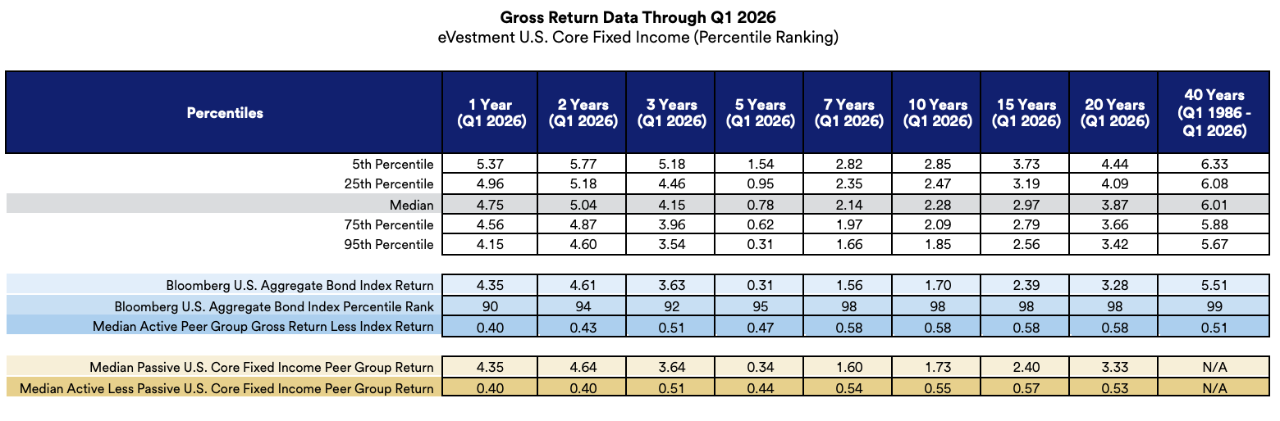

Comparing the Bloomberg U.S. Aggregate Bond Index with the eVestment U.S. Core Fixed Income manager universe over a full market cycle suggests active management has historically offered a stronger case in fixed income than in many areas of equity investing.

Across annualized trailing periods over the last 40 years, the Bloomberg U.S. Aggregate Bond Index — which is not available for direct investment, but is replicated by many passive managers — ranked in the bottom decile of the eVestment U.S. Core Fixed Income manager universe. Over those same trailing periods, the median actively managed composite outperformed both the index and the median passive composite by approximately 40 to 58 basis points (bps) annually on a gross-of-fee basis. It also outperformed both the index and the median passive composite by roughly 21 to 39 bps per year on a net-of-fees basis.

The peer group consists of all composites, entries, products, and/or strategies in eVestment self-identified as belonging to the U.S. Core Fixed Income universe. This universe is defined as U.S. Fixed Income products that invest in a well-diversified investment grade bond portfolio, most commonly allocating to treasury, corporate, securitized, and government-related issuers. Common benchmarks for the universe include the Bloomberg Barclays U.S. Aggregate and Bloomberg Barclays U.S. Govt/Credit.

Short-term underperformance can occur, especially in times of extreme volatility. The U.S. Aggregate Bond Index has matched or exceeded the return of the median eVestment U.S. Core Fixed Income composite in 11 of 40 calendar years since 1986.

The most extreme example was 2008, when the index outperformed the median active composite by 187 bps before fees. Even then, roughly one-third of active composites still outperformed the index, and the median active composite outperformed the index by 369 bps before fees in 2009.

Institutional investors should assess results over full market cycles, although excessive tracking error over shorter periods can still provide useful risk management insights. They should also decompose returns to determine whether excess performance came from repeatable skill or from unintended risks.

The Role of Passive Management

Passive strategies can be useful for highly liquid government bond exposures, short-term tactical allocations, or situations in which cost minimization and low tracking error are the overriding objectives. They may also serve as temporary vehicles for cash equitization or broad beta exposure.

By nature, they are largely bound to index rules, making them less compelling as the default solution for complex institutional investment grade portfolios. As credit risk, liquidity management, liability alignment, unique investment constraints, and downside protection become more important, the case for active management strengthens.

Conclusion

Fixed income markets are fragmented, structurally complex, opaque, and heavily influenced by credit quality, liquidity, interest rates, and benchmark construction. Those characteristics create meaningful opportunities for active managers to add value and manage risk.

Passive strategies play a role in parts of the investment grade market but also have structural weaknesses. Active management, by contrast, allows institutional investors to pursue credit selection, duration positioning, liquidity management, downside protection, and portfolio construction aligned with unique client objectives.

For institutional investors, the question is whether generic benchmark exposure is sufficient for the portfolio’s purpose. When liabilities, liquidity needs, credit risk, regulatory or accounting constraints, or downside protection matter, active management offers advantages that extend well beyond simple benchmark outperformance. Even with higher potential fees, the long-term performance of active management is compelling.

In that context, the structural characteristics of investment grade fixed income make the case for active management as the more effective approach for sophisticated institutional investors.

For questions about this report, please reach out to your relationship manager.