Why Consider Asset-Backed Securities Now?

April X, 2026

Defining Asset-Backed Securities (ABS)

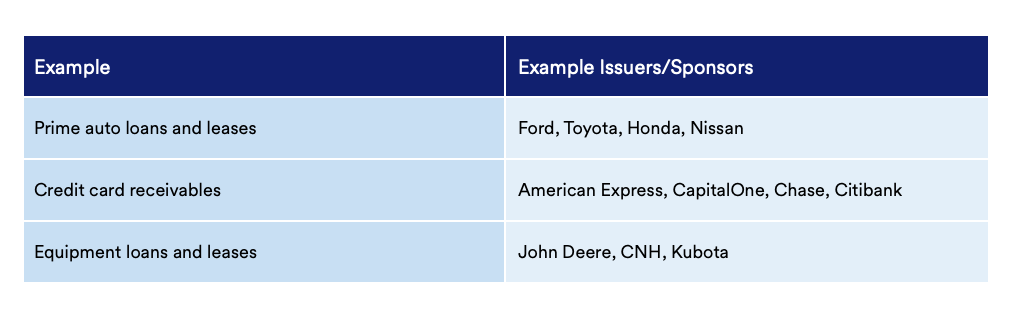

ABS are notes backed by underlying pools of financial assets such as automobile loans and leases, credit card receivables, equipment loans and leases, student loans and others used by a diverse investor base. Some investors prefer securities with a longer duration or a higher yield that might be more esoteric in nature with lower liquidity. Meanwhile, others may prefer securities with shorter cash flows, higher credit quality and a higher degree of liquidity. In this discussion, we will focus our comments on the latter, which includes prime auto, credit card and equipment receivables.

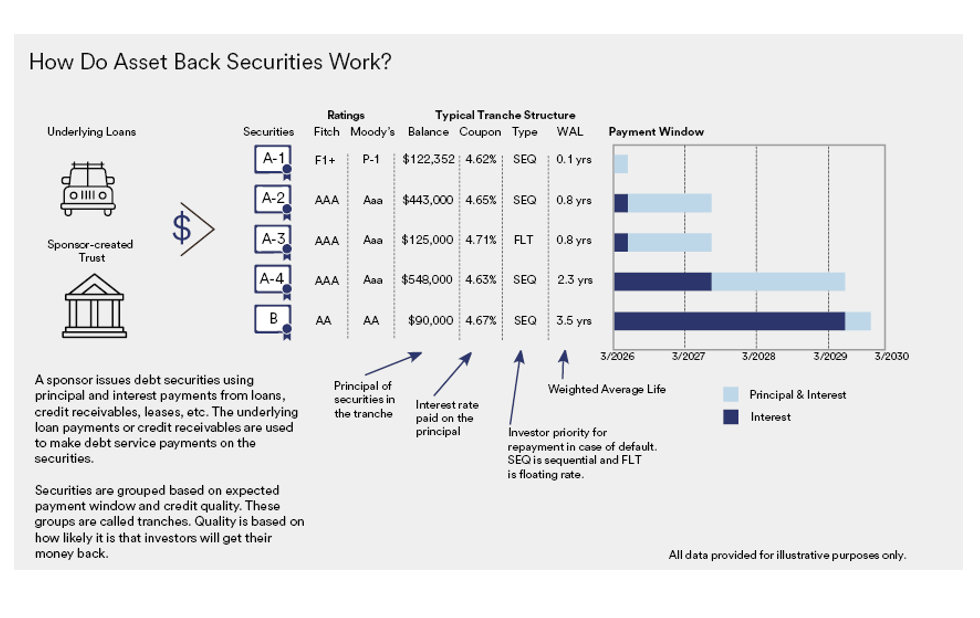

While some ABS might have a “bulleted” structure, where the principal is paid at maturity, most ABS deals comprise multiple classes of securities, or “tranches,” each with a different coupon, expected cash flows, and risk characteristics and they pay principal and interest on a monthly basis. Asset-backed securities can serve as a component of fixed-income portfolios, offering investment diversification and the opportunity for higher yields relative to comparable-duration U.S. Treasuries and other government securities.

An ABS structure includes three key parties: the sponsor, the trust and the investor. In most cases, the sponsor — a bank, credit card issuer or retail finance company — transfers the loans or receivables to a separate trust, which is established to legally own and securitize the assets. The trust then issues the ABS notes and is responsible for paying principal and interest in a timely manner.

Key Characteristics of ABS

1. Credit Enhancements. Unlike most corporate securities, ABS are typically credit-enhanced, which means they contain features that raise their credit quality above that of the underlying assets. Credit enhancement increases the likelihood that investors will receive the promised cash flows and is typically designed to provide a loss buffer equal to a multiple of historic loss experience.

The following are examples of credit enhancements:

Excess Spread — the first layer of protection from underlying asset losses and is comprised of the difference between the interest rate on the underlying collateral and the bond coupon and deal costs.

Cash Reserve Account — additional funds set aside by the issuer to provide extra internal liquidity for ABS investors.

Overcollateralization — the amount of collateral in excess of ABS notes issued. Overcollateralization is generally non-declining.

Senior/Subordinate Structure — subordinated tranches absorb losses due to defaulted loans up to their value before senior tranches are affected. As a result, subordinate tranches typically offer investors a higher yield due to their increased credit risk. This feature provides investors with the option to invest in a tranche that best suits their preferences and risk tolerance.

Additionally, while not a type of credit enhancement, the underlying collateral portfolios are generally designed to be well-diversified with low allocations to individual loans/borrowers and geographic regions. This is designed to mitigate widespread portfolio deterioration during times of stress.

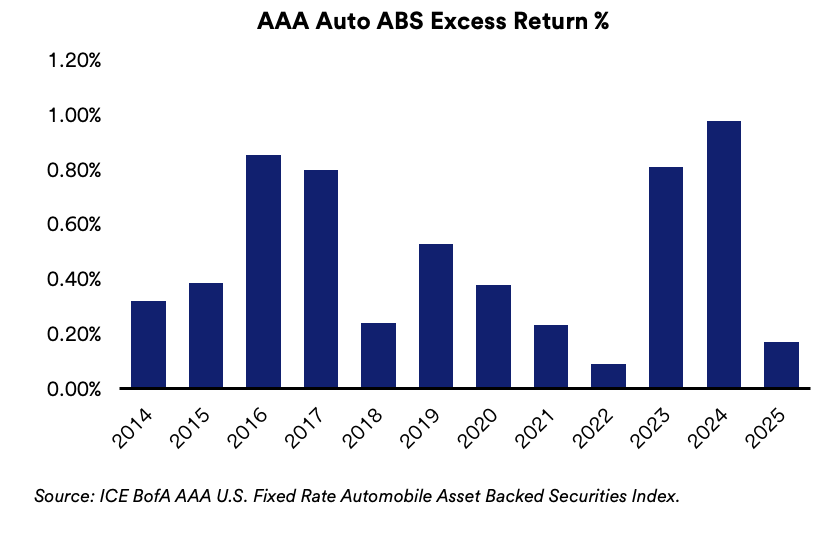

2. Potential to Add Value Over Time. ABS is an asset class that can potentially offer a high degree of safety with returns in excess of those of duration-matched Treasury bonds and higher risk-adjusted returns compared to other sectors. The chart below shows excess returns (or the additional return over a comparable duration treasury) for an index of AAA rated autos.

3. Large and Liquid Market. ABS issuance was $374 billion in 2025, modestly below the elevated pace seen in 2024. Of this total, $178 billion came from autos, credit cards, and equipment. The market is liquid, with the average trading volume for the ABS market around $2.1 billion in 2025, reflecting continued strong investor participation.

Our Approach to ABS

We conduct a credit review and monitoring process specifically for ABS, going beyond simply accepting assigned ratings and instead focusing on the structure, collateral quality, credit enhancements and history of the parties to the deal. Further, we focus on sponsors who issue securities primarily to provide efficient funding for core businesses as opposed to issuers who use it to enhance returns or lay off risk. This process includes a review of the sponsor, the historical performance of similar deals (especially the default and recovery rates), an analysis of the collateral, underwriting criteria, geographic diversification of the pools and other considerations.

Additionally, our credit team conducts or reviews stress tests that assess the effectiveness of credit enhancements in protecting the tranches we would consider purchasing. After a purchase is made, we monitor the issue to ensure its performance meets expectations, and we conduct monthly surveillance on all ABS owned in our clients’ portfolios. We focus on deals that offer the combination of features desired by our clients: high-quality credit profile, safety characteristics, and relative value to other sectors.

Why Now With ABS?

Investors have long considered ABS to be a secure and profitable addition to fixed-income portfolios. With the tightening of spreads across sectors which have long been a mainstay of public sector portfolios, such as federal agencies and investment-grade corporates, high quality alternative investments like ABS are becoming important sources of incremental income and diversification for investors.

There has been concern expressed about the state of the American consumer especially those in low to moderate income brackets. Because ABS are backed by auto loans and credit cards, an increase in unemployment could lead to increased delinquencies or defaults. While some increase in losses and delinquencies is a possibility, we believe the credit enhancements discussed earlier should provide sufficient protection to avoid impairment on senior tranches of these securities.

Adding ABS provides another investment option for high-quality portfolios, allowing us another opportunity to help enhance returns and diversify portfolios for our clients..

For more information about this report, please contact your relationship manager.

Sources

Securities Industry and Financial Markets Association (SIFMA)

ICE BofA AAA U.S. Fixed Rate Automobile Asset Backed Securities Index