Domestic Banks: Third Quarter Rundown

August X, 2025

We believe that thoughtful credit investing begins with a deep understanding of the sectors we invest in. To share how we approach this, we’re providing a multi-part series that explores key industries shaping today’s credit landscape. Each installment will highlight the sector-specific dynamics we’re monitoring and the factors influencing our investment decisions.

We begin with domestic banks, authored by Rob Hajduch, Managing Director of our Taxable Credit Research team. With more than 30 years of industry experience, Rob brings a seasoned perspective on how evolving fundamentals and regulatory shifts are shaping credit opportunities in the banking space.

A Quick Sector Overview

Earnings performance in the domestic banking sector in 2024 was refreshingly uneventful after the dislocations that followed highly publicized regional bank failures in 2023. Stable operating performance carried into the first half of 2025, defying expectations of deposit attrition, driving a liquidity squeeze, and asset quality deterioration related to inflation expectations and elevated interest rates.

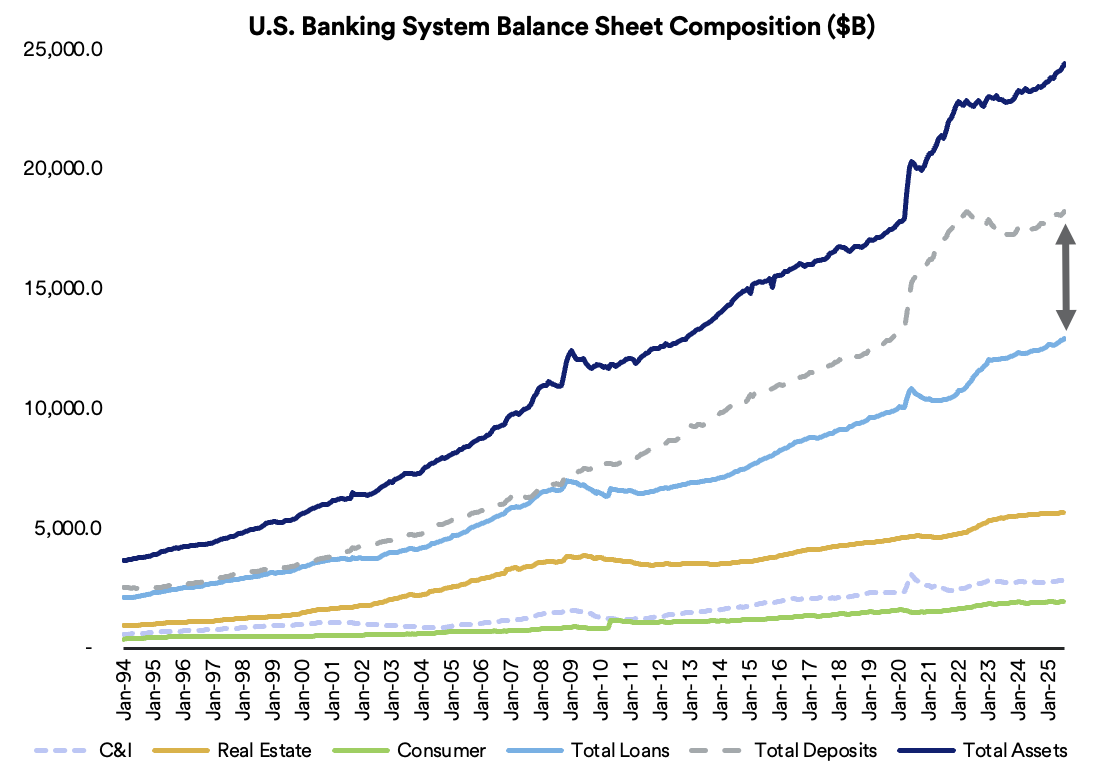

The following chart sourcing Federal Reserve (Fed) industry data illustrates the system’s balance sheet positions from early 1994 through mid-July 2025. The gap between total deposits and total loans represents excess liquidity in the system. Not only has the system not experienced an erosion in deposits, but the base has also grown by $263.7 billion with deposit balances exceeding total loans by $5.3 trillion.

Source: Federal Reserve Board (FRB).

Our Outlook

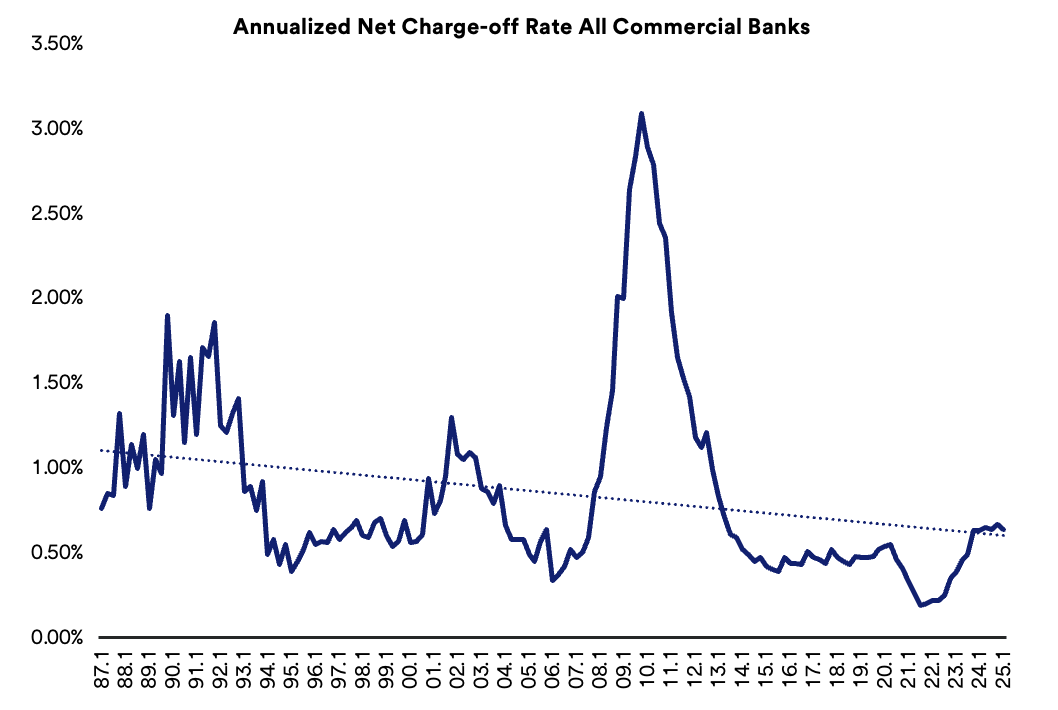

Despite loan losses rising from the post-pandemic lows, asset quality stabilized in 2024 through the end of the first quarter of 2025. The long-term trend for total net charge-offs in the system since 1987 moreover is positive, as illustrated in the following chart.

Source: Federal Reserve.

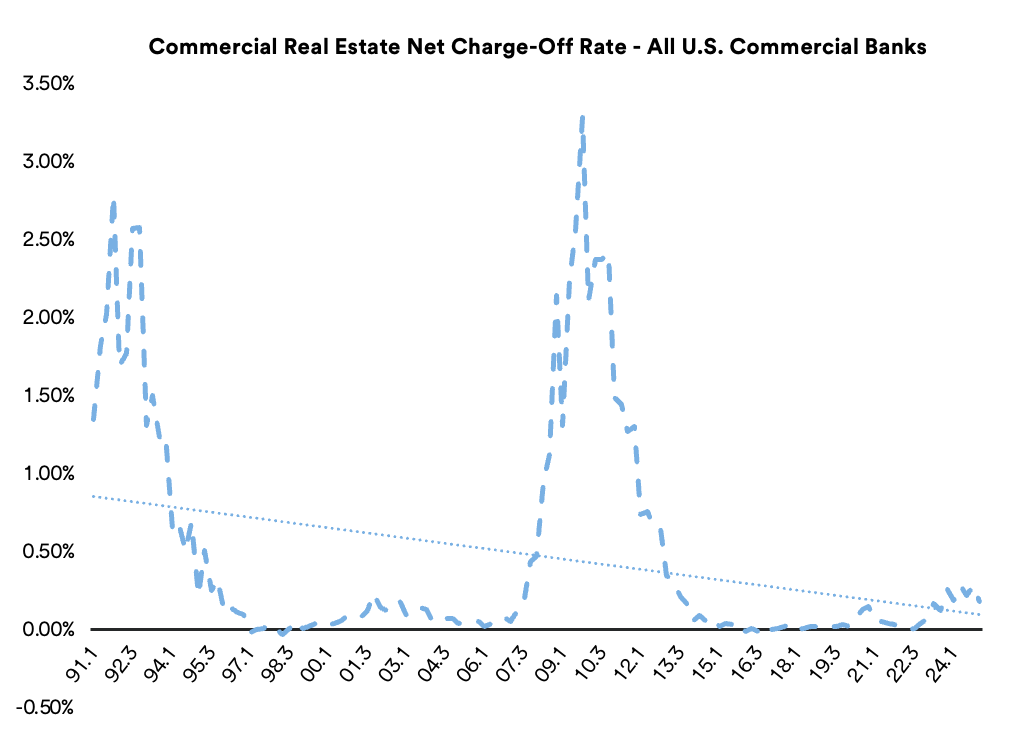

Headlines notwithstanding, even commercial real estate (CRE) is not exhibiting the anticipated stress from slow return to office mandates and elevated refinancing costs. The annualized net charge-off rate for CRE across the banking system was 0.18% in the first quarter of 2025, with losses moving higher incrementally to a level roughly equivalent to that reported for the first quarter of 2004. The long-term trend since the Federal Reserve began tracking CRE asset quality is also positive.

Source: Federal Reserve Board (FRB).

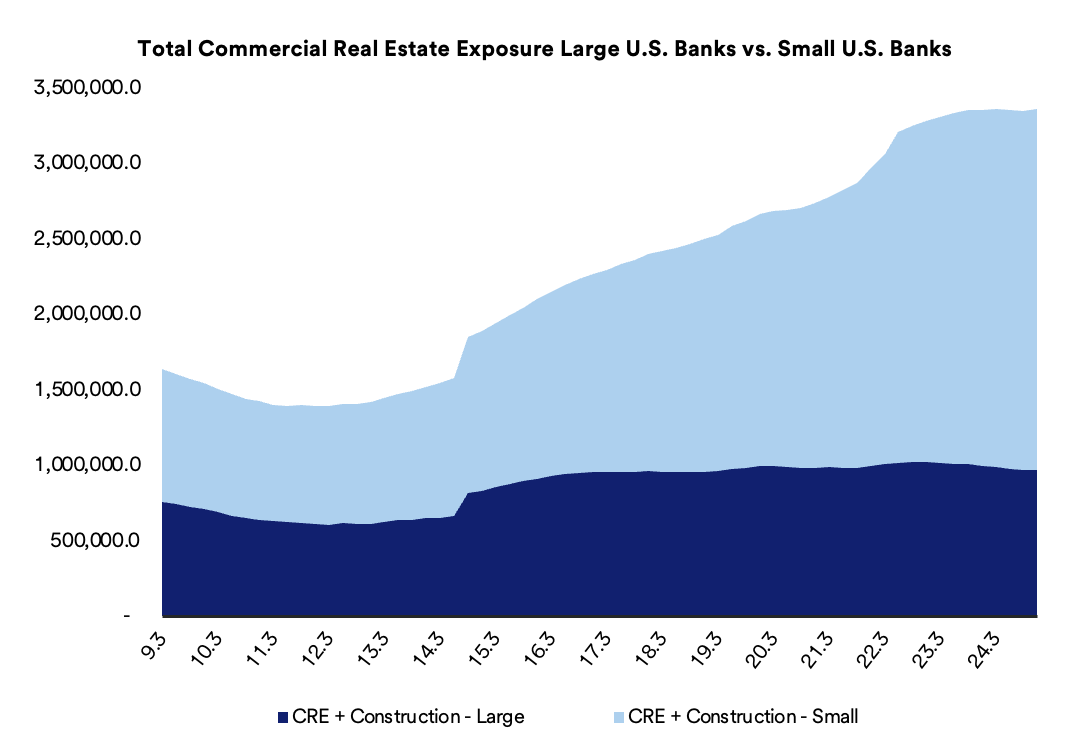

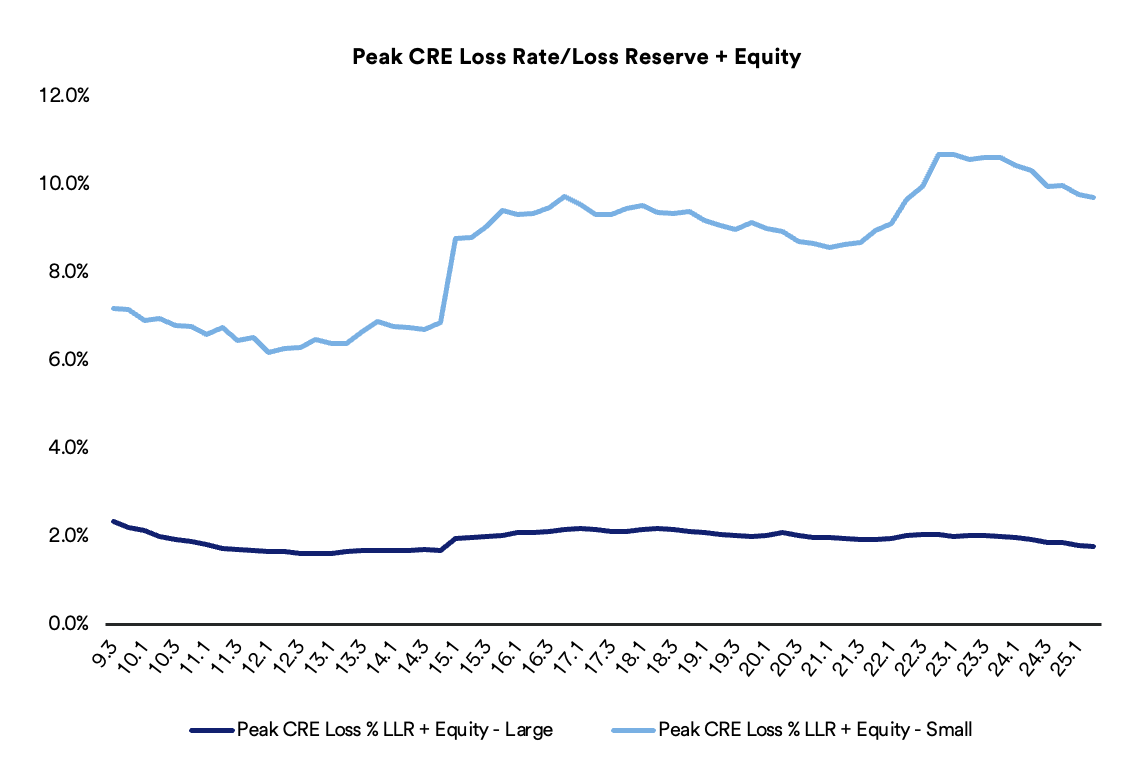

Even if losses in CRE were to spike to levels touched during the Global Fiancial Crisis, most of the banking system’s exposure is held by small banks that are not actionable as they do not fund in the capital markets. Even those banks appear to have sufficient loss reserves and capital to manage through the current cycle. Small banks account for 71% of toal CRE loans in the system, with CRE representing over 52% of total loans in their portfolios. Large banks’ loan portfolios are more diversified, with CRE exposure equivalent to 13.5% of their loan portfolios at the end of the second quarter of 2025.

Source: Federal Reserve Board (FRB).

Assuming a constant 3.28% peak loss rate equal to that experienced by the system in the fourth quarter of 2009, the large bank cohort would lose 1.8% of their total loan loss reserve and balance sheet equity. Small banks would suffer a more painful but still manageable loss of 9.7% of their loss reserve and balance sheet equity. Consequently, we do not view CRE expsoure as a systemic existential threat, and those banks that do fail are likely to be idiosyncratic events driven more by inadequate underwriting, poor risk management, or — as has been the case with a number of recent failures — fraud.

Source: Federal Reserve Board (FRB).

Conclusion

Taken together, the U.S. banking system continues to benefit from a deep liquidity profile; stable loan asset quality, even in problematic categories; and reserve and capital positions sufficient enough to manage through the current credit cycle. Accordingly, we remain comfortable with investment in the large U.S. regional and systemically important banks.

Should you have any questions about this report, please reach out to your relationship manager.

In our next piece, we will outline some of the big issues impacting the pharmaceutical space.