Aerospace & Defense: Flying on Momentum

November X, 2025

To provide an understanding of how we think about various credit sectors, we produced a series of pieces that outline significant issues impacting sectors including domestic banks, pharmaceuticals, and technology. In part four of this four-part series, Kim Troedsson, Principal Credit Analyst, discusses the risks and opportunities associated with the aerospace and defense sector.

A Quick Sector Overview

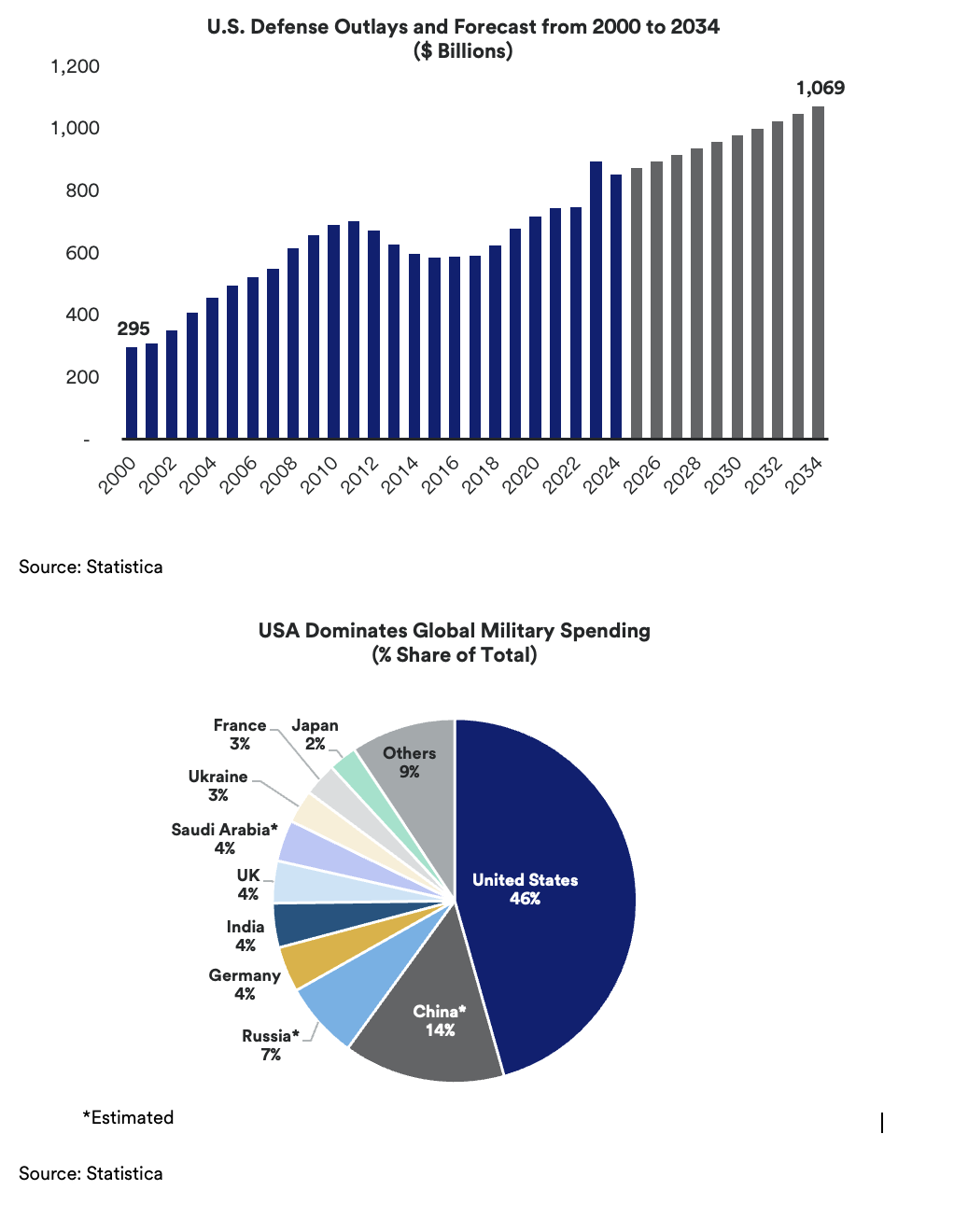

The Aerospace & Defense (A&D) sector encompasses products and services for both commercial and government markets. These companies produce some of the world’s most technologically sophisticated commercial aircraft, fighter jets, bombers, helicopters, missiles and air defense systems, submarines, aircraft carriers, tanks, ground vehicles, and munitions. Some companies enjoy significant revenues from foreign purchasers, while others depend almost entirely on the U.S. government. The U.S. is the world’s largest market for A&D, accounting for almost half of global 2024 spending (see table below).

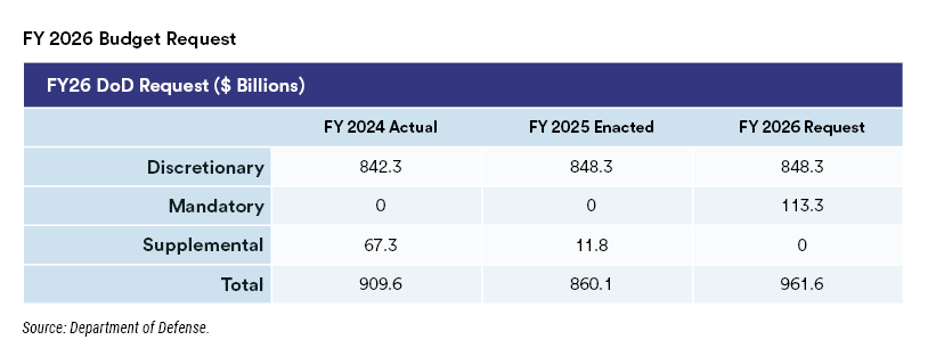

Sector demand remains strong, and some product programs can extend for several years with then ongoing revenue streams from needed maintenance and logistical support post product delivery. Commercial airlines are seeking to upgrade their fleets as commercial air travel grows, while defense companies are benefitting from growing global defense budgets fueled by security threats posed by China, the Middle East, and the war between Russia and Ukraine. The Department of Defense’s fiscal year 2026 budget request of $962 billion represents an 11% spending increase over fiscal year 2025.

A&D companies’ sales backlog is typically over two year’s revenue while commercial aircraft order books extend out for years. Yet delivering on these orders is challenged by persistent supply chain bottlenecks, skilled labor shortages, and company-specific issues, while inflation continues to push costs higher. Tariffs may present an additional disruption as visibility on the future effects of tariffs is limited given their fast-evolving framework and questions over who will ultimately bear associated costs. Tariffs are likely to be higher for commercial aerospace than for defense because of the latter’s higher strategic importance and more localized supplier base.

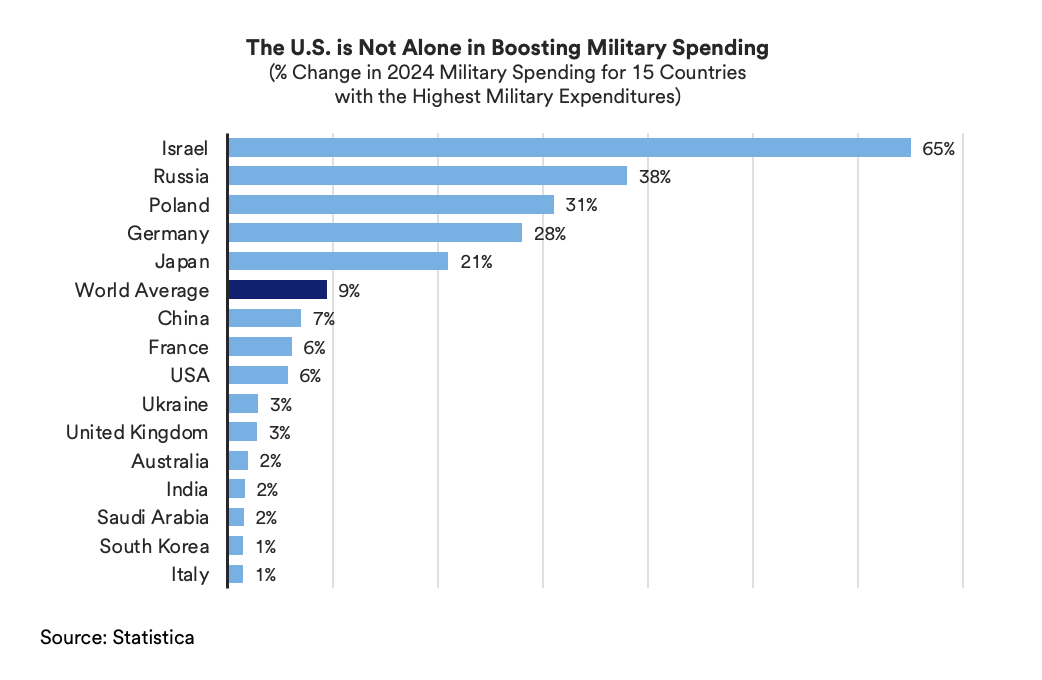

The defense spending outlook is robust for the U.S. with a steady upward trajectory for military outlays. But the U.S. is not the only country feeling the heat from rising global threats. Military spending for other countries is also set to increase driven by rising threats in their regions (see charts below) and perception that they must take on more responsibility for ensuring their own security.

Our Outlook

We hold a favorable outlook for the A&D sector with its strong order books for commercial aircraft and increasing global defense spending. Demand momentum is translating to solid revenue visibility for two years or more for large aerospace and defense companies. Though inflationary costs may pressure margins, these higher costs should be partially offset by efficiency initiatives and contract price increases. We expect operating earnings and cash flow growth exempting any unforeseen issues which may arise from negative contract revisions or product problems requiring remediation spending. Though supply chain constraints and skilled labor shortages may slow production, we don’t believe such delays will overcome the underlying strength of the sector.

Though it appears there’s “something for everyone” in the current environment, we are focusing on the largest companies with substantial sales backlogs and diversified revenue streams, whose product and services expertise matches to Department of Defense spending priorities; these include manufacturers focused on shipbuilding to increase the size of the Navy fleet with a focus on autonomous technologies. Other budget priorities will benefit those companies with expertise to participate in a nascent Golden Dome missile defense initiative, which includes space-based technology. Others to benefit include companies providing land-based battlefield equipment and munitions to replenish the federal arsenal and expand production as well as satisfy elevated demand from NATO allies.

While these companies’ revenue streams are set to be bolstered by robust demand, U.S. government budgets have yet to be given the green light by congress. If reduced, however, the budget is still likely to exceed the previous fiscal year. Earnings may disappoint if supply chain deliveries fall short or software or hardware defects emerge. Though inflationary cost increases will present a challenge, operators will partially offset the impact through price increases as well as cost control measures.

Conclusion

Strong demand for A&D products and services is driving the outlook for continued growth in operating income and cash flow for the sector. We expect that large A&D companies, with their diversified operations, large sales backlogs, and technological expertise, will benefit despite pressures from inflation, supply chain constraints, and potential execution mistakes. Some companies are in prime position to benefit from initiatives specifically targeted in the government’s fiscal 2026 budget proposal and we are focused on those producers where budget approval is likely to be a catalyst for higher investment values.

If you have any questions about this report, please reach out to your relationship manager.