Part 1: How Smaller and Mid-Size Endowments Can Benefit from the Endowment Model

September X, 2025

Part 1: How Smaller and Mid-Size Endowments Can Benefit from the Endowment Model

The endowment model is a well-known investment approach to asset allocation used by large endowments and foundations. The basic principle behind the endowment model is to allocate a significant portion of the portfolio to alternatives such as private equity and diversifying strategies. This approach has historically been implemented by the largest university endowments, however there are fewer barriers to entry today for smaller endowments and foundations — particularly when those entities work with an experienced outsourced chief investment officer (OCIO) firm.

But before delving into how smaller endowments and foundations (E&Fs) can take advantage of this strategy and potentially use alternative assets to enhance returns over time, we will, in a two-part series, first provide additional detail about the endowment model itself. Second, we will list the advantages and disadvantages associated with alternative strategies.

Endowment Model 101

Based on the book “Pioneering Portfolio Management,” which was published in 2000, the endowment model is often referred to as the “Yale Model” and was developed at Yale University by its one-time Chief Investment Officer, David Swensen, and Dean Takahashi, its senior endowment director. The idea behind the endowment model is to allocate heavily to private capital illiquid strategies to harvest long-term illiquidity premium that would deliver outsized performance over public markets over a longer horizon, while diversifying long-term portfolio risk.

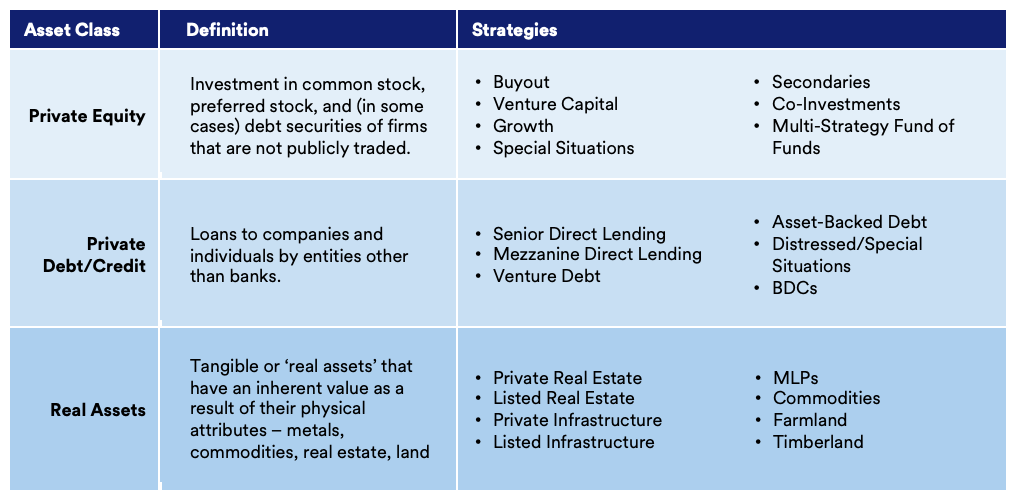

Private Capital Strategies

Private capital (or private markets) strategies encompass various strategies such as private equity, venture capital, private debt/credit, and others. Private capital strategies are illiquid because the funds are invested over three to five years and then harvested after seven to 10 years. Thus, the client/investor loses access to these funds until fund maturity or distribution as they are locked up over the life of the investment. For larger endowments, this allocation can top 50% or more of their portfolio.

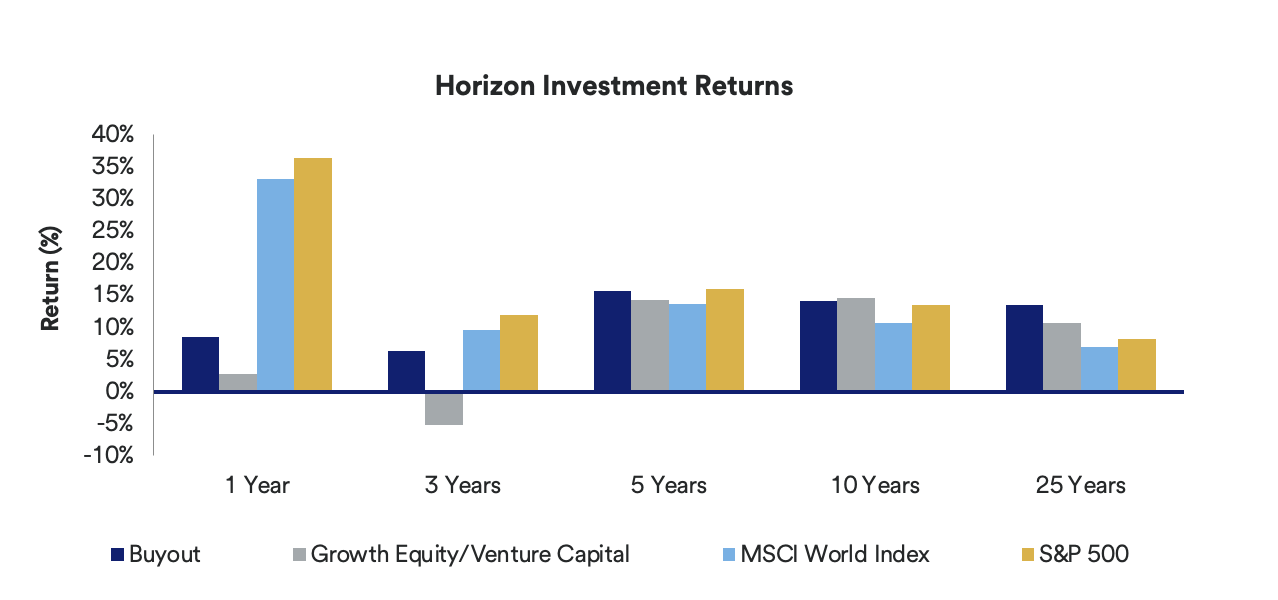

Many endowments have benefited through this approach over the years because private capital has historically provided investors with opportunities to increase portfolio diversification and returns. Exhibit 1 on the next page shows the outperformance of private equity over S&P 500 over 3-, 5-, 10-, and 25-year horizons. In addition, private capital provides portfolio diversification, particularly with diversifying strategies, through less correlated assets which reduce risk and improve risk adjusted returns.

The following chart shows returns for private equity versus public equity over a 25-year time horizon.

Source: McKinsey Global Private Markets Report 2025

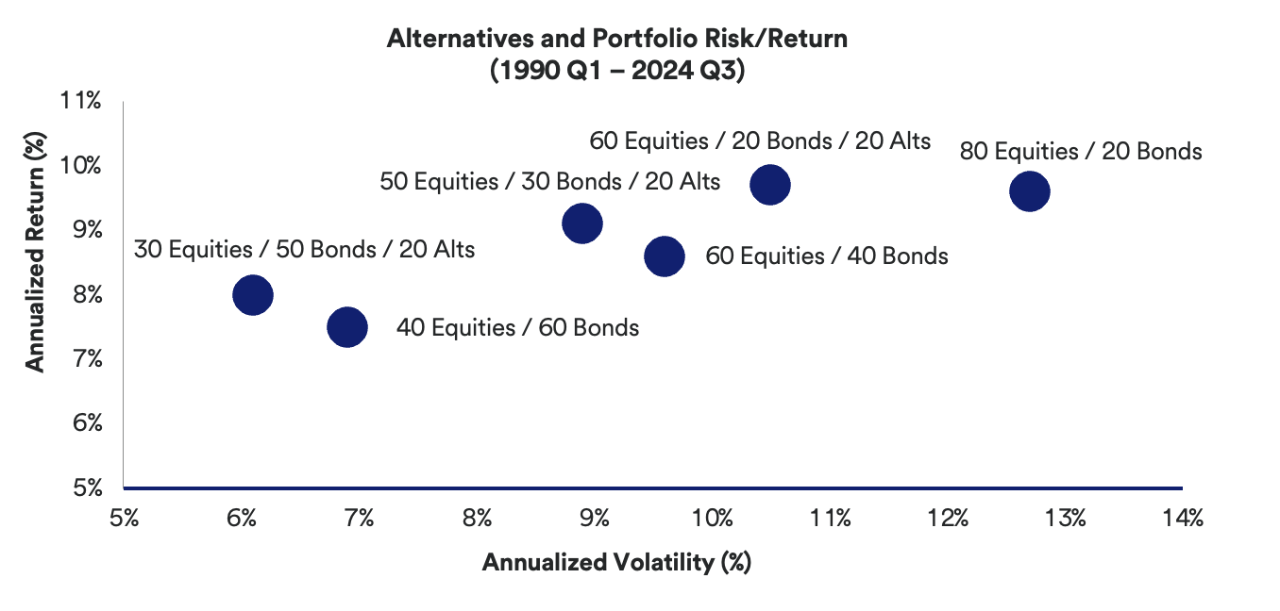

The following chart shows how adding to alternatives can reduce risk and improve risk-adjusted returns.

Source: JPMorgan Guide to Alternatives 2025 Q1

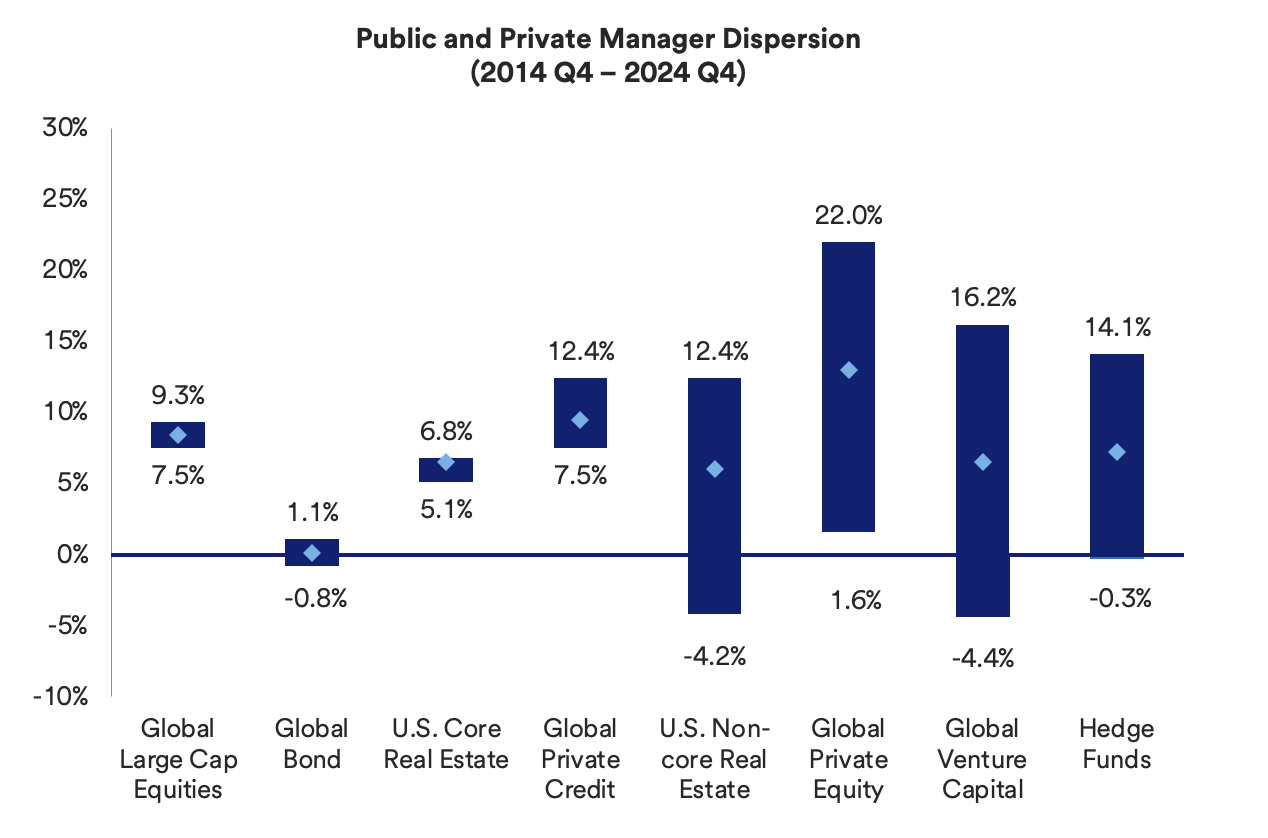

Another important consideration about private capital strategies is the dispersion of returns, which measures the difference between the highest performing managers and the lowest performing managers. The dispersion of returns is significantly higher than the dispersion of returns for public markets strategies. This implies that, on average, returns for public markets between top and bottom managers are relatively close to each other, whereas returns for private capital have a large difference between best-performing funds and worst-performing funds. The implication for investors is that they need access to better performing funds.

Source: JPMorgan Guide to Alternatives 2025 Q1

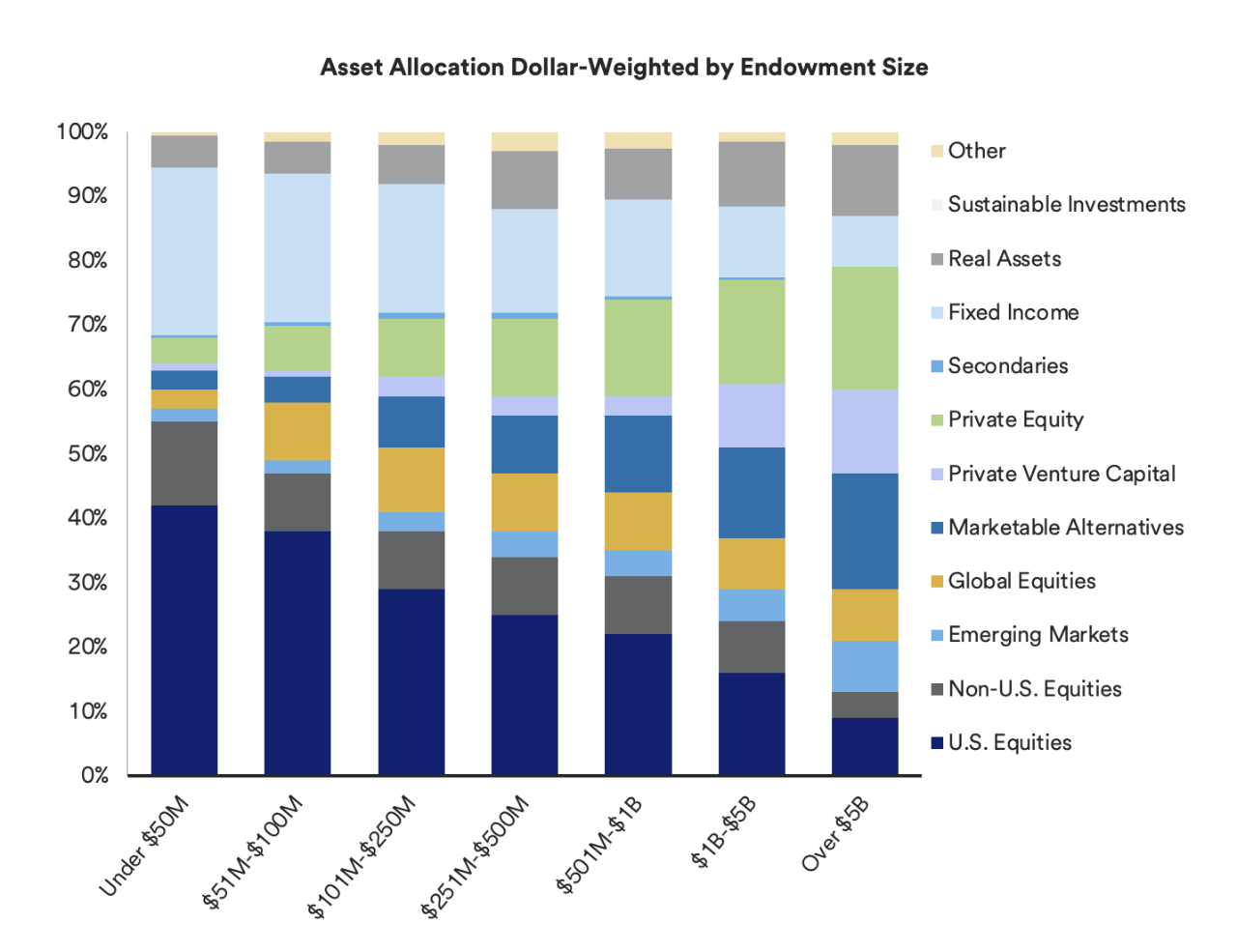

Why Smaller Endowments Have Not Been Taking Advantage of Alternative Investments

Historical barriers have limited small- and medium-sized endowments from accessing larger allocations to alternative investments. Larger endowments, simply due to their size, have less sensitivity to illiquidity, thus they can allocate larger percentage amounts to illiquid private capital. Saying it in a different way, larger endowments allocate larger absolute amounts to the institution’s budget, even though the percentage allocation to the budget may be similar to smaller endowments.

According to the 2024 NACUBO-Commonfund Study of Endowments, larger endowments also have a greater percentage of funds allocated to private capital than smaller endowments, which historically provided better long-term portfolio performance. The unintended effect is that smaller and midsize endowments compensate for this by having a larger public equity allocation, thus potentially driving up portfolio risk.

The chart below shows how larger endowments allocate more to private capital and smaller endowments allocate more to public equity.

Source: 2024 NACUBO-Commonfund Study of Endowments

Because larger endowments allocate larger absolute amounts to private capital than smaller endowments and because they often have internal investment teams, they can potentially decrease due diligence time and allocate faster, which makes them more attractive to private capital managers. This in turn drives private capital managers to seek out larger endowments, resulting in self-selection between larger endowments and better-performing managers.

Also, because larger endowments have been implementing the endowment model longer, they have developed longer and more enduring relationships with private capital managers.

Lastly, because larger endowments allocate larger amounts to private capital, they need to have a larger universe of private strategies to invest in. At the same time, because there are more funds in a portfolio, larger endowments take more risks with smaller and emerging private capital managers. Although the risk is higher for these managers, diversifying across many smaller and emerging managers can promote higher overall performance, albeit with higher longer-term risk, which larger endowments can endure.

To summarize, the smaller and mid-size endowments would allocate smaller percentages and smaller absolute amounts to private capital due to manager access and research resources, which in turn precludes them from accessing top-tier managers. This is an inherent challenge for smaller endowments as they have smaller amounts to allocate and less buying power, which reduces their access to top private capital strategies.

For questions about this report, please reach out to Alex Gurvich at alex.gurvich@usbank.com or your relationship manager.

Stay tuned for part two of this two-part series. In the coming piece we will discuss how small endowments might think about using alternatives within their portfolios and talk more about how those entities might be well-served by enlisting the services of an outsourced chief investment officer (OCIO) firm.

Sources

- 2024 NACUBO-Commonfund Study of Endowments

- JPMorgan_Guide to Alternatives_2025 Q1

- McKinsey Global Private Markets Review 2025

Glossary of Private Capital Alternative Investments Definitions