Conflict in the Middle East - Implications for Inflation, Growth, and Financial Markets

March 25, 2026

Recent developments involving Iran have understandably raised questions from clients about potential impacts on markets and portfolios. Periods of heightened geopolitical risk often bring uncertainty, rapid news flow, and short‑term market volatility, making it challenging to interpret market signals.

In this note, we address the most common questions we are hearing from clients — including what is happening, why it matters for the global economy, how markets have responded to date, and how we are evaluating portfolio positioning in this environment. We remain focused on assessing how evolving risks may affect inflation, growth, and financial conditions, and how these factors influence execution of our disciplined decision-making process.

What is happening, and why does it matter for markets?

Aside from the humanitarian toll, military action involving Iran has triggered significant disruptions in global oil supplies and other key commodities, raising the risk of higher inflation and slower global economic growth. Financial market reactions have been noticeable yet largely contained, with daily volatility reflecting the evolving nature of the situation. Current market pricing suggests that investors view further significant escalation as unlikely, though uncertainty remains elevated.

At this stage, we do not believe it is prudent to make significant portfolio changes based on predictions about the timing or resolution of the conflict.

Why is Iran so important to global energy markets?

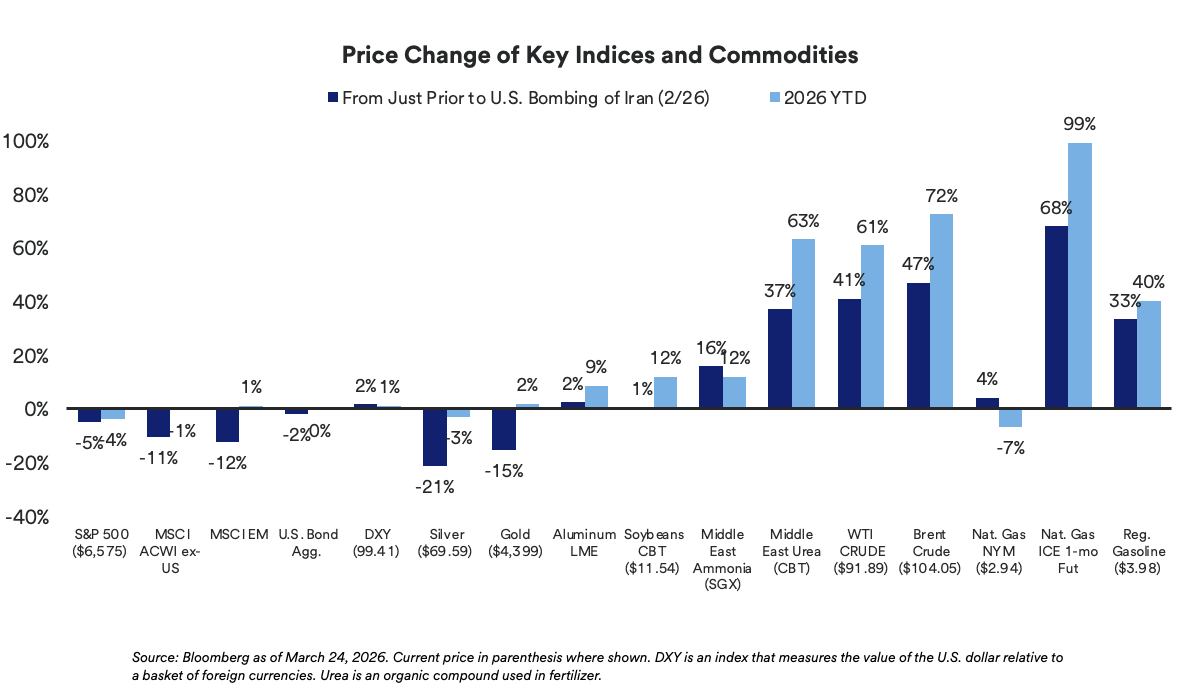

Iran plays an outsized role in global energy markets not only because of its oil production and export capacity, but also due to its strategic geographic position. Approximately 20% of global oil flows through the Strait of Hormuz, making even partial disruptions economically significant. Recent military actions and attacks on energy infrastructure across the Gulf region have disrupted global supply chains, driving oil and other commodity prices materially higher.

The chart below reflects the price action observed across major energy and commodities markets since February 26, just before the military action.

How are higher energy prices affecting the economic outlook?

Higher energy prices are already permeating the broader economy. The key macroeconomic question investors are now asking is how long these elevated energy prices will persist.

A sustained increase in energy prices effectively acts as a tax on consumers and on energy‑importing economies and businesses, slowing economic growth while simultaneously pushing headline inflation higher. As a result, markets remain focused on whether energy‑driven price pressures stay contained or begin to spill over into other categories, such as core goods and services. Ultimately, the ultimate economic impact will depend heavily on the duration and extent of supply disruptions, which remain highly uncertain.

What does this mean for Federal Reserve policy and interest rates?

The conflict complicates an already challenging policy backdrop for the Federal Reserve (Fed). Policymakers must assess whether energy‑related inflation pressures could broaden at a time when the labor market has been cooling and inflation remains elevated above the Fed’s 2% target.

In response to recent developments, futures markets have eliminated expectations for near‑term Fed rate cuts, while Treasury yields have risen across the curve, with short‑ and intermediate‑term yields reaching eight-month highs. These moves reflect heightened policy and inflation uncertainty rather than a material shift in long‑term growth expectations.

How have equity and credit markets responded so far?

Outside of commodities, capital markets have generally processed developments in an orderly fashion. U.S. equities have declined but have not experienced a full market correction, while international equities have faced greater pressure given their higher reliance on Middle East energy supplies. Credit spreads have widened modestly from historically tight levels but remain narrow, supported by solid corporate fundamentals.

What are the risks if the conflict escalates or persists?

If disruptions to energy supply persist or intensify, inflation pressures could increase further while global growth risks rise, including the potential for recession in energy importing regions. Under such a scenario, consumers and businesses would face higher costs, corporate earnings expectations could be revised lower, and risk assets could experience additional volatility. These risks underscore why uncertainty and risk premia remain elevated across markets.

What does this environment mean for fixed income portfolios?

Higher yields across the Treasury curve have improved income opportunities within fixed income. In select accounts, we have viewed the recent cheapening in rates as an opportunity to lock in higher yields and, where appropriate, modestly extend duration. Similarly, wider credit spreads have created opportunities to add selectively in certain sectors while maintaining strict diversification and risk management standards. Portfolio adjustments are being made tactically, guided by our long-standing disciplined portfolio management process rather than in response to short‑term headlines.

What does this environment mean for multi-asset class portfolios?

Given the high degree of uncertainty and the difficulty of forecasting geopolitical outcomes, we are not making broad portfolio shifts based on assumptions about the conflict’s duration or resolution. Instead, we remain focused on disciplined portfolio construction, diversification, and incremental opportunities created by higher yields and modestly wider spreads. We will continue to closely monitor developments and assess portfolio strategy based on evolving risks to inflation, growth, and financial market stability.

For additional information regarding this report, please reach out to your relationship manager.