Introduction to Our OCIO Investment Process: Strategic Asset Allocation Framework

Our outsourced chief investment officer (OCIO) investment team is committed to delivering multi-asset-class solutions that seek to add value for clients through asset allocation and manager selection, disciplined portfolio construction, and robust governance. As part of our three-part series on the OCIO investment process, the first paper introduced the four pillars of our approach: governance; strategic and tactical asset allocation; vehicle selection; and portfolio implementation. In this second paper, we discuss the foundational building blocks of our strategic asset allocation framework — the central pillar of the investment process.

For each client seeking to generate long-term returns, we develop a strategic asset allocation framework that outlines expected return and risk characteristics across intermediate- and long-term horizons. To build well-diversified portfolios, the framework incorporates equities, fixed income, listed real assets, and alternatives (including private capital strategies). Return and risk expectations derived from our Capital Market Assumptions are used to align portfolios with client return requirements and risk tolerance levels.

When establishing strategic asset allocation targets with clients, we incorporate long-term return expectations, volatility, and correlations as core inputs to portfolio construction. In our view, the decision to include an asset class in a multi-asset-class portfolio should not be based solely on absolute return expectations; it should also reflect the underlying drivers of return and risk, as well as how the asset class fits within the broader portfolio. Focusing only on short- to intermediate-term differences in absolute returns can lead to concentrated portfolios and reduce portfolio resilience over time.

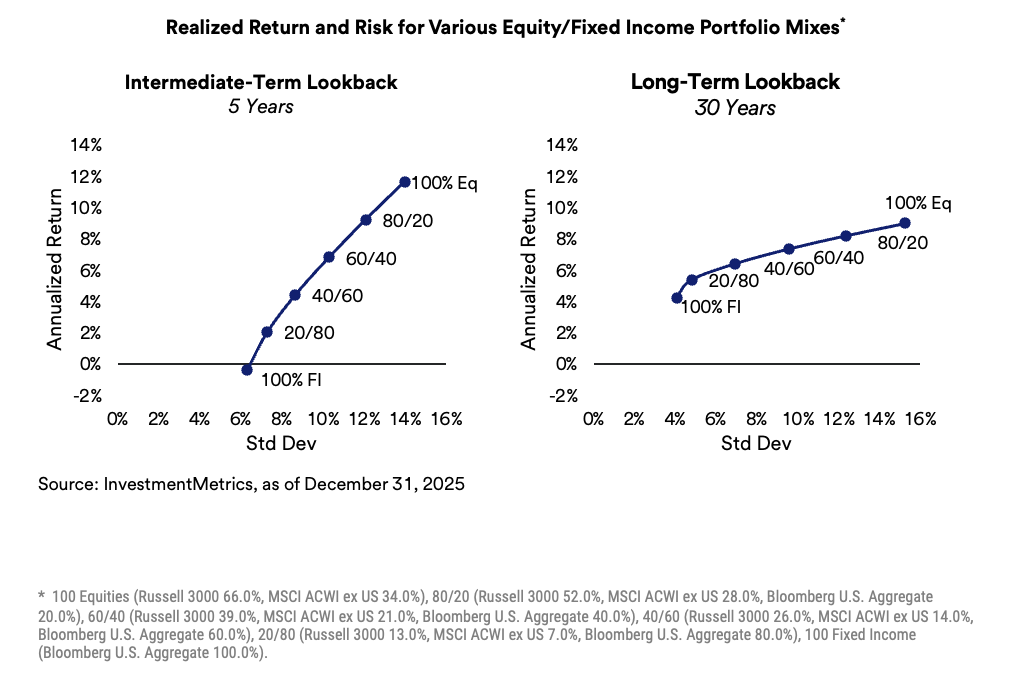

Fixed income serves as the ballast of a portfolio, providing principal preservation qualities and predictable, stable income returns. Equities provide the critical capital appreciation potential necessary for investors to meet their long-term return objectives. By combining equities and fixed income in varying proportions, investors can construct multi-asset portfolios designed to align with long-term risk and return objectives as seen in the chart below.

While the chart above focuses solely on equities and core fixed income, our strategic asset allocation framework includes more granular level target allocations to domestic equity, international equity, core fixed income, below-investment-grade fixed income, and listed real assets. Where appropriate based on a client’s return objectives, liquidity profile, and investment restrictions, the framework may be expanded to include alternatives. The sections below summarize key themes we consider when developing a strategic asset allocation plan for clients. The third installment in this series will outline the criteria we use for manager selection across these asset classes.

Core Fixed Income: Critical Role in Principal Preservation and Stable Income Return

Inclusion of fixed income within multi-asset portfolios is critical for principal preservation characteristics and steady income returns. Our portfolio construction process emphasizes allocation to domestic core fixed income markets over international fixed income markets that bring in the additional complexities of currency translation and liquidity issues. Domestic fixed income markets offer exposure to some of the largest and highest quality fixed income issuers in the world. This was evident in the performance following the global financial crisis. For the 20 years ending March 31, 2026, Bloomberg Global Aggregate ex USD has returned 1.71% (annualized), while Bloomberg U.S. Aggregate has returned 3.28% (annualized).

Global Equity Allocation: Allocations Across Domestic and International Equity

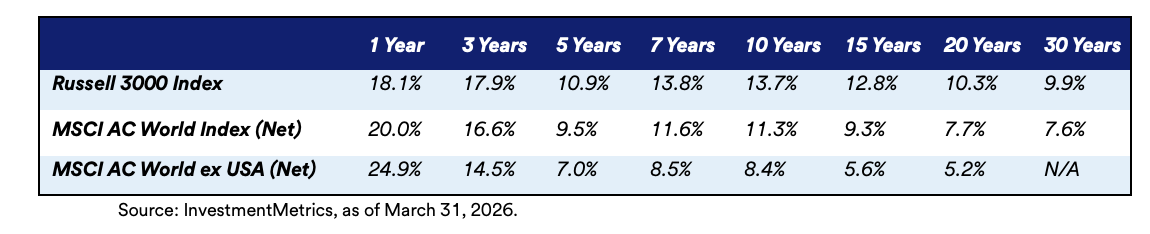

Our strategic portfolio maintains dedicated allocations to domestic and international equities, rather than a single global equity allocation, to reflect different characteristics and performance drivers across these markets. U.S. equities have significantly outperformed international equities since the 2008 global financial crisis, supported by higher profit margins, more consistent earnings growth, and greater exposure to growth-oriented corporate sectors—an advantage that persisted through much of the past decade. However, leadership has not been consistent over time. During the early 2000s, for example, international equities outperformed domestic equities for extended periods, including from 2001 through October 2007 and again from late 2008 through mid-2009. This latter period coincided with the S&P 500 Index trading broadly flat from 2000–2009, a stretch sometimes referred to as “the lost decade.” Separating domestic and international equity allocations enables us to reflect evolving market leadership while preserving flexibility for tactical asset allocation.

Domestic equities make up 63% of the global equity benchmark today (MSCI ACWI Index, as of March 31, 2026). Our strategic split between domestic and international equities is in the two-thirds to one-third ratio, reflecting the composition of global equity benchmarks. This focus on global market cap breakdown allows us to avoid exhibiting any structural home country bias or international equity bias into the portfolio construction process.

Domestic Equity: Strategic Design Aligned with Market Cap Structure of U.S. Stock Market Universe

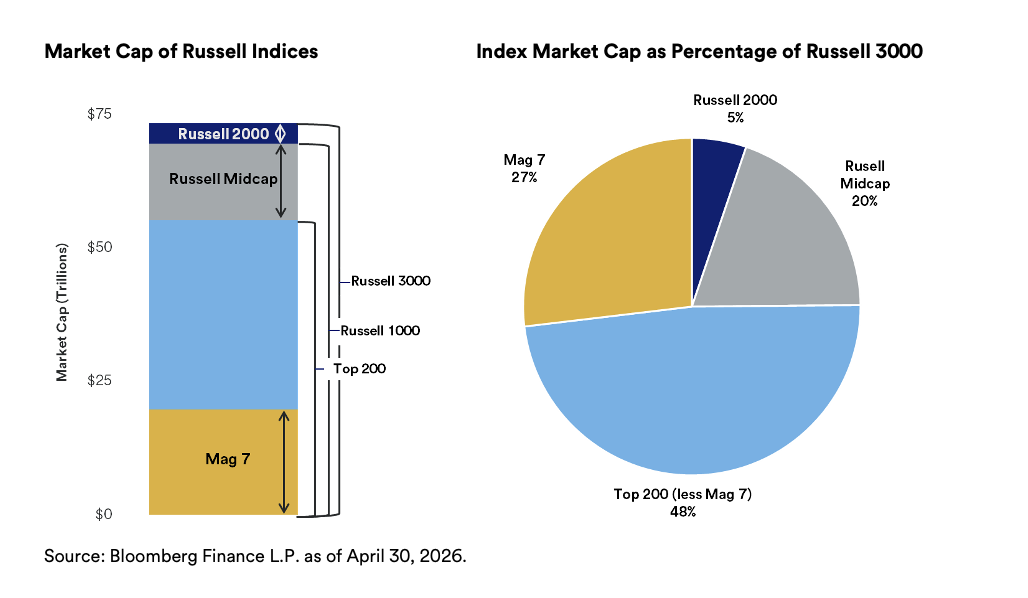

Our domestic equity strategic design aligns with the market cap definitions of the Russell 3000 Index. Based on our 20+ years of OCIO experience,1 we believe the Russell 3000 Index is the most comprehensive representation of domestic equities, representing approximately 98% of the investable U.S. stock market universe. We maintain a strategic allocation to the large- and mid-cap components of the Russell 3000 Index which represent approximately 95% of the index as measured by market cap. Additionally, we maintain a strategic allocation to U.S. small-cap stocks represented in the Russell 2000 Index, which comprise approximately the remaining 5% market cap of the Russell 3000 Index.

Consistent use of an index family that aligns with the capitalization structure of the U.S. equity market eliminates structural biases in our portfolios and reduces unintended overlapping stock exposures introduced by cross-pollinating multiple index families. Additionally, our market-cap-based strategic design with the stock universe breadth of the Russell 3000 Index offers an effective and efficient structure to express tactical asset allocation views.

Role of Below-Investment-Grade Credit within Multi-Asset Portfolios

The below-investment-grade (high yield) bond universe has grown significantly and currently stands at approximately $1.5 trillion—about 13% of the $11.5 trillion U.S. corporate bond universe—and accounted for 17% of total trading volume in 2025. Credit quality within the high-yield universe has also improved over time; for example, the J.P. Morgan High Yield Bond Index currently has approximately 40% in B and CCC ratings versus roughly 60% prior to the global financial crisis. In addition, high yield has exhibited a correlation of 0.52 to core fixed income for the 10 years ended March 31, 2026. In our view, high-yield credit has evolved from a primarily tactical allocation to an asset class that warrants a dedicated strategic allocation, reflecting its differentiated qualities and benefits in portfolio construction.

Diversification Benefits of Listed Real Assets Allocation

Market conditions and the inflationary environment in 2022 reinforced that volatility and shifting correlations can negatively affect portfolio outcomes. To help mitigate these risks, we include a strategic allocation to listed real assets—equally weighted between U.S. real estate investment trusts (REITs) and global listed infrastructure—to enhance downside characteristics, reduce equity-driven volatility, and add inflation-sensitive exposure with lower volatility and carrying costs than certain other real asset categories (e.g., commodities).

Since the global financial crisis, correlations between global equities and public real assets have generally been elevated. However, for the 10 years ended March 31, 2026, the data still indicate diversification benefits: correlations for U.S. REITs and global infrastructure versus global equities were 0.79 and 0.77, respectively. In a potentially higher inflation environment, a diversified real assets allocation should be additive to portfolio outcomes.

Conclusion

Strategic asset allocation is the single most important input to long-term portfolio outcomes, and bridges long-term client objectives into a diversified portfolio structure informed by return expectations, risk, and correlations. By establishing dedicated, strategic allocations across domestic and international equities, core fixed income, below-investment-grade credit, and listed real assets—and incorporating private alternatives when appropriate—we seek to build portfolios that are resilient across market and economic cycles. In the next installment of this series, we will outline our manager selection criteria and how we implement these asset-class allocations through both passive and active strategies that are consistent with the overall portfolio design.

If you have any questions about this report, please contact your relationship manager.

Notes

1 First discretionary OCIO client dates to August 2000. OCIO experience includes legacy organizations.