Latest Endowment Study Shows Broad Gains Across the Board in FY 2025

March 23, 2026

Strong Investment Returns Continue to Propel Endowments

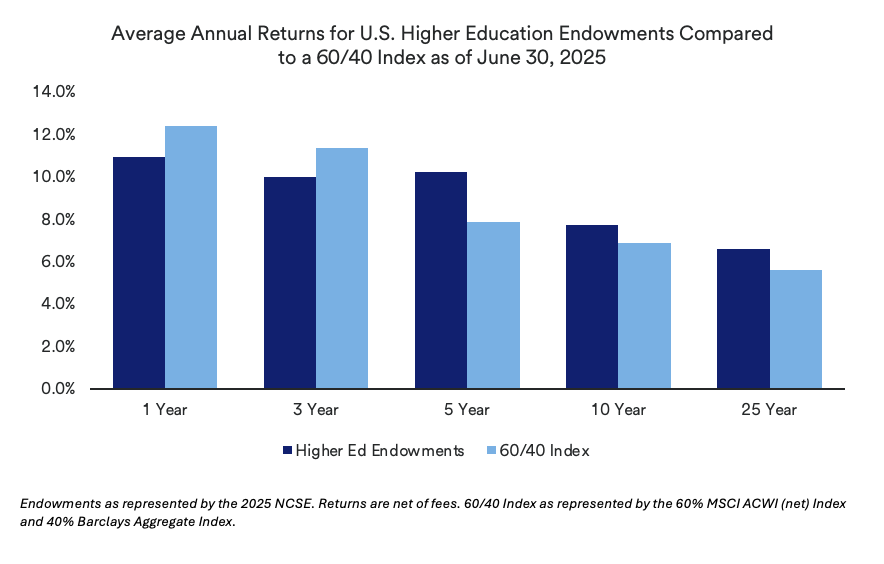

Endowment returns continued to outperform a 60/40 portfolio over the long term despite ongoing market volatility. Integrating alternative strategies, which offer diversified return streams from non-correlated assets classes, often serves to moderate volatility and support overall performance. For the trailing 5-, 10-, and 25-year periods ending June 30, 2025, endowments outpaced the 60/40 index.

According to the 2025 NACUBO-Commonfund Study of Endowments (NCSE), U.S. higher education endowments generated an average return of 10.9% for the fiscal year (FY) ended June 30, 2025. While this is slightly below last year’s 11.2%, it marks the third consecutive year of double-digit gains. All seven endowment cohorts (by size) achieved double-digit returns, with the largest cohort earning 11.8%. Return dispersion narrowed meaningfully — 130 basis points (bps) versus 390 bps the year prior. Longer-term results improved as well: 10-year annualized returns rose to 7.7%, and 25-year returns increased to 6.6%.

When compared with a balanced 60/40 portfolio (60% MSCI ACWI (net) Index, 40% Barclays Aggregate Index), endowments lagged in both 1- and 3-year periods — 10.9% versus 12.4% and 10.0% versus 11.35%, respectively. This short-term outperformance of the 60/40 benchmark can be partly attributed to its heavier allocation to public equities within the MSCI ACWI. With public equities delivering strong results again this year, that overweight meaningfully boosted the index’s performance.

Strong Investment Returns Continue to Propel Endowments

Endowment returns continued to outperform a 60/40 portfolio over the long term despite ongoing market volatility. Integrating alternative strategies, which offer diversified return streams from non-correlated assets classes, often serves to moderate volatility and support overall performance. For the trailing 5-, 10-, and 25-year periods ending June 30, 2025, endowments outpaced the 60/40 index.

According to the 2025 NACUBO-Commonfund Study of Endowments (NCSE), U.S. higher education endowments generated an average return of 10.9% for the fiscal year (FY) ended June 30, 2025. While this is slightly below last year’s 11.2%, it marks the third consecutive year of double-digit gains. All seven endowment cohorts (by size) achieved double-digit returns, with the largest cohort earning 11.8%. Return dispersion narrowed meaningfully — 130 basis points (bps) versus 390 bps the year prior. Longer-term results improved as well: 10-year annualized returns rose to 7.7%, and 25-year returns increased to 6.6%.

When compared with a balanced 60/40 portfolio (60% MSCI ACWI (net) Index, 40% Barclays Aggregate Index), endowments lagged in both 1- and 3-year periods — 10.9% versus 12.4% and 10.0% versus 11.35%, respectively. This short-term outperformance of the 60/40 benchmark can be partly attributed to its heavier allocation to public equities within the MSCI ACWI. With public equities delivering strong results again this year, that overweight meaningfully boosted the index’s performance.

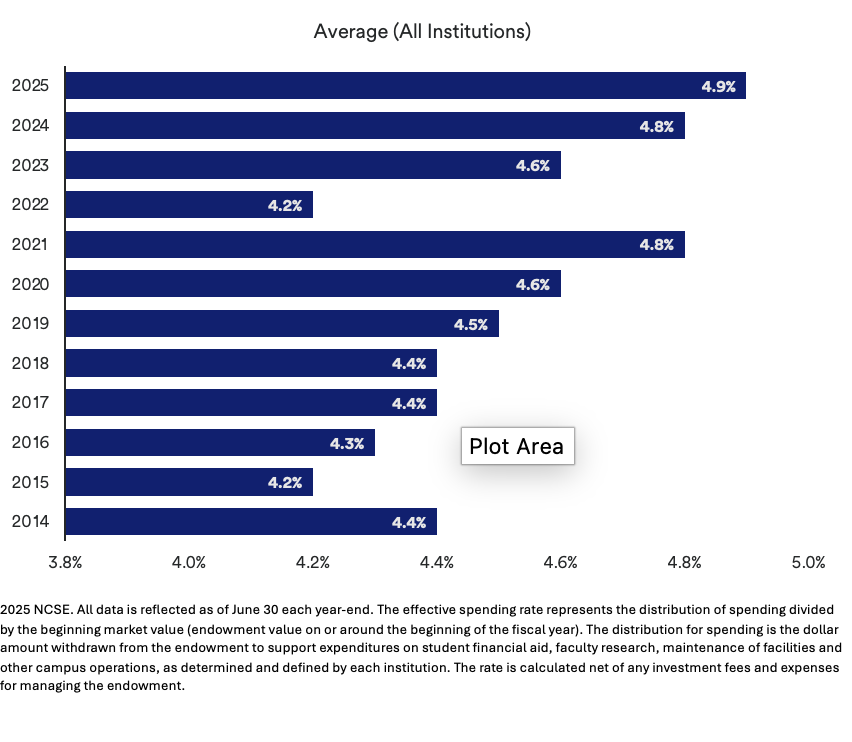

U.S. college and universities increased endowment spending to more than $33 billion to help stabilize operations and support students, faculty, and the school’s mission. Across all institutions, student financial aid represented the largest share of spending policy distributions in FY 2025 at 47.4%, while campus operations and maintenance accounted for the smallest share at 7.6%. In total, academic programs and research, endowed faculty positions and “other” collectively made up the remaining 45% of spending.

Asset Allocation

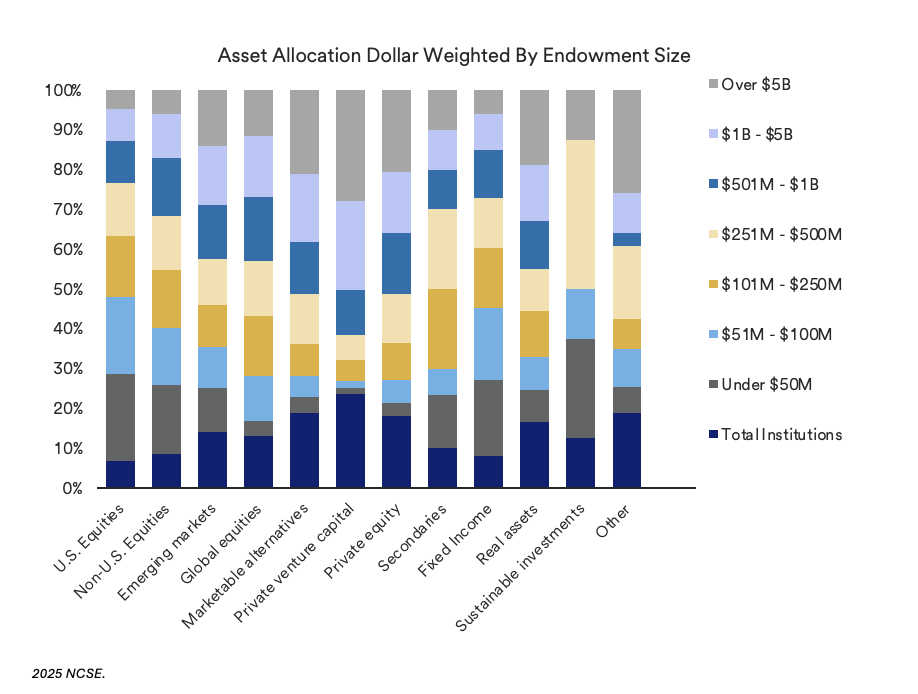

FY 2025 marked the third consecutive year in which U.S. equities (both active and passive) led all asset classes in performance. Smaller endowments — those with assets under $50 million — allocated 44.0% to U.S. equities, compared with just 11.6% for endowments over $5 billion. This higher allocation benefited smaller institutions over the three years ending FY 2025, during which they achieved an average annual return of 11.5%, versus 7.8% for the largest endowments. Larger endowments tend to maintain greater exposures to alternative investments, which have historically generated stronger long-term returns than public market securities.

Responsible Investing Still a Conundrum

In FY 2024, 82.5% of institutions responding to the study reported including environmental, social, and governance (ESG) considerations in their investment policies. Across stakeholder groups — students, alumni, employees, donors, and grant makers — interest in ESG investing continues to grow albeit gradually. Yet 63.7% of respondents indicated that they still do not practice responsible investing in any form.

Notably, 58.8% of institutions in the largest surveyed cohort viewed responsible investing as a potential source of alpha, compared with 24.6% of the smallest endowments — nearly double the 13.5% reported in FY 2024. However, implementation of ESG, SRI, and Impact Investing strategies continues to face meaningful challenges. According to the 2025 study, 31.9% of respondents cited pooled fund structures (including private investments) as a barrier to implementation. Another 33.4% expressed concern about potential adverse impacts on investment performance, while 27.2% pointed to potential conflicts with the board’s fiduciary duty to ensure mission sustainability.

Among institutions that reported practicing responsible investing, nearly 60% relied on an outsourced chief investment officer (OCIO) to implement their programs.

OCIO Model Preferred by Many

For colleges and universities with limited time, staff and resources, the OCIO model can help relieve the administrative burden of managing an endowment. In the FY 2025 results, 57.3% of respondents with endowments of $500 million or less reported using an OCIO, a figure consistent with the percentage seen in the FY 2024 results.

Top Concerns Shows New Reality

The study once again asked participating institutions to identify their top two concerns from a list of nearly 20 choices — a line of inquiry first introduced in FY 2024. Respondents selected their top two without ranking them.

The number one concern, cited by 23.8% of respondents, was student enrollment. It was identified at more than twice the rate of the second most common concern, fundraising, which was selected by 11.5% of respondents. When examining the same data across the endowment-size cohorts, the largest endowments were most concerned about federal funding cuts (28.6%), followed by liquidity (14.3%). Notably, federal funding cuts were not an option in last year’s survey. The top concern in FY 2024 was liquidity at 16%.

Our View

As institutions continue to navigate an evolving and uncertain market environment — with expectations for challenged investment returns in the intermediate term but improvements over the long term — it remains critical to keep investment and spending policies current while being mindful of the costs associated with managing the investment program. In light of the latest NCSE study findings, here are several considerations:

· Revisit target asset allocation. As demands on endowment funds Increase, institutions may want to reassess their target asset allocation to ensure portfolios are positioned appropriately given expectations for returns, inflation, and the fees associated with their endowment program.

· Evaluate active versus passive exposures. After three strong years in the domestic equity market, this may be an opportune time to review the mix of active and passive exposures across asset classes. A quick analysis of manager-return dispersion can help indicate whether active management is likely to add value. Low dispersion suggests limited opportunity for alpha, while high dispersion indicates that alpha may be available and worth pursuing through active strategies.

· Review public and private equity allocations. With the recent rise in public equities, private equity valuations have become more compelling in certain segments. An updated allocation review between public and private equity may be timely.

· Monitor fees and vendor contracts. Costs are one of the few factors that can be directly controlled, and they should be reviewed regularly. Institutions should consider evaluating all external vendor contracts related to the endowment to ensure fees remain reasonable and appropriately support the endowment’s objectives.

· Refresh board education plans. Managing expectations is a critical component of successful endowment oversight. After several years of strong returns, it may be beneficial to revisit the board’s education plan to reinforce the cyclical nature of investment returns and the importance of maintaining disciplined, prudent portfolio positioning.

If you have any questions about this report, please reach out to your relationship manager.

Sources

https://www.nacubo.org/Research/2025/NACUBO-Commonfund-Study-of-Endowments.