Q&A – The ABCs of Asset-Backed Commercial Paper

February X, 2026

To gain a better understanding of asset-backed commercial paper, a security commonly utilized in short-term fixed income portfolios as part of a diversified strategy, we conducted a Q&A session with Jeff Rowe, CFA. Jeff is head of portfolio management for liquidity products for our investment advisory team.

Before we dive into ABCPs, in simple terms, what is traditional commercial paper (CP)?

Rowe: Traditional commercial paper is a type of short-term investment with a maturity date from one to 270 days. For over a century, corporations have used commercial paper to finance current transactions or working capital needs, such as a company’s payroll, inventory, and accounts payable. Over the years, CP has become an important component of fixed income debt markets and has grown, per Federal Reserve data, to over $1.3 trillion outstanding as of December 31, 2025.1

In terms of structure, commercial paper is considered unsecured, meaning it is not backed by collateral, and its repayment is dependent on the issuer. Therefore, it is important to assess the creditworthiness of the issuer when purchasing commercial paper.

What is ABCP and what makes it different than traditional commercial paper?

Rowe: Similar to traditional commercial paper, asset-backed commercial paper is a type of short-term investment which typically has a maturity date between one to 270 days. The market for these instruments was developed to provide additional short-term funding and liquidity to financial institutions and corporations.

Unlike traditional commercial paper, ABCP is secured or backed by collateral. A special purpose entity (SPE) purchases a pool of financial assets, such as credit card receivables or auto loans. The cashflows received from these pooled financial assets are distributed to investors.

The SPE is typically set up by large global financial institutions on behalf of its clients including financial institutions and corporations. These clients are attracted to sell their loans into a SPE to free up their balance sheet and get short-term funding at attractive rates.

ABCP has a broad base of investors and broker-dealers and can even be more liquid than certain unsecured CP programs. ABCP typically provides incremental yield relative to unsecured CP from the same or a similar sponsoring institution.

What are the main structures of ABCP available today?

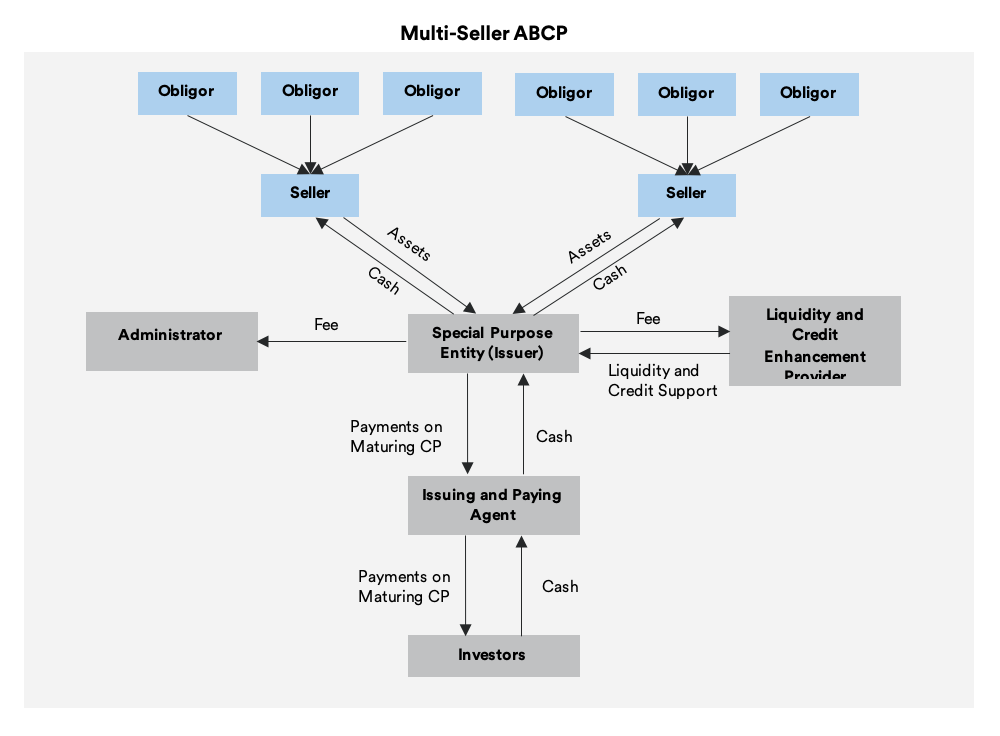

Rowe: The most common type of ABCP structure is called multi-seller. In a multi-seller program, the SPE buys financial assets from different financial institutions. Multi-seller programs are considered diversified since they contain a variety of loans with different credit risk profiles. The following are the key parties in a multi-seller ABCP structure:

- Obligor: Original borrowers of the loans used as collateral. For example, for credit card receivables, the obligors would be the credit card holders.

- Seller: Financial institutions or corporations who originated the loans that are sold into the SPE.

- SPE: A legally separate entity that purchases the financial assets and issues the ABCP.

- Liquidity and Credit Enhancement Provider: Parties that can improve liquidity and credit enhancements.

- Administrator: Oversees the day-to-day operations including, reviewing the performance of the assets and communicating out to investors.

- Issuing and Paying Agent: Holds the account that receives the proceeds of newly issued ABCP and makes repayments to the ABCP investors

- Investors: Owners of ABCP.

What are the liquidity and credit enhancements for ABCP programs?

Rowe: ABCP typically benefits from liquidity and credit support provided by banks affiliated with the transaction, which tend to be large global financial institutions.

The form of credit and liquidity support differs and is dependent upon the structure of the program. For a multi-seller program, there are three support mechanisms in place to protect investors from credit and liquidity risk:

Transaction-Specific Credit Enhancement: This is the first line of defense against any losses that arise from the asset pool. Transaction-specific credit enhancement is usually designed to cover a multiple of historical losses and can be achieved through overcollateralization, excess spread, cash reserve, guarantees or a line of credit:

- Overcollateralization occurs when there are more underlying assets to repay the ABCP than there is debt outstanding. This provides credit enhancement because defaults are first absorbed by the excess assets before impacting underlying ABCP holders;

- Excess spread is when the borrowing rate on the underlying assets exceeds that of the ABCP. This provides credit enhancement because the excess interest inflows can be used to offset defaults that may occur;

- A cash reserve is a fund established to make ABCP investors whole in the event of defaults on the underlying assets; and

- Guarantees and lines of credit are provided by third-party entities who are obligated to varying degrees to make ABCP investors whole.

Program-Wide Credit Enhancement: This covers residual credit losses that are not absorbed by transaction-specific credit enhancements. The SPE enters into an agreement with a bank, under which the bank covers any credit-related losses not covered by the transaction-specific credit enhancements. These program-wide credit enhancements are typically sized to 5-10% of the ABCP outstanding.

Liquidity Risk: Addressed by a liquidity facility that can be drawn upon in case of a mismatch of cash flow between assets and liabilities or market disruption. Liquidity facility and program-wide credit enhancements are usually provided by the same bank.

Because of these features, ABCP programs are typically rated by at least two of the three largest Nationally Recognized Statistical Rating Organizations (NRSROs). Nearly all ABCP currently in the marketplace is in the top rating tier.2

What are the main risks of investing in ABCP?

Rowe: While short-term investments usually carry low interest rate risk due to their short maturities, investing in ABCP adds an element of credit risk, or the risk that the ABCP issuer does not ultimately pay its obligation when it comes due. Another risk is liquidity risk, or the risk that you may be unable to easily sell CP prior to its maturity at a fair price. Downgrade risk, or the risk that a rating agency may downgrade the rating of a CP holding negatively affecting its market value and liquidity, is another potential risk. Interest rate risk, or the risk that the market value of a CP holding may fluctuate based on changes in interest rates, must also be considered, although the short-term maturity of ABCP makes it typically less susceptible than longer-term investments.

Additionally, given the unique structure of ABCP, investors must perform rigorous due diligence focusing on a variety of factors including the underlying assets and source, the parties in the transaction, and the credit enhancement and liquidity support.

How do you manage the risks of ABCP programs?

Rowe: As described in detail in part one of this Q&A series, our Credit Research Group, and its dedicated credit research analysts, is responsible for determining approved credits, including ABCP, for our various approved lists. When evaluating the suitability of an ABCP program, our team examines the experience of key parties (sponsor, administrator, support provider), nature of liquidity and credit support, legal structure and flow of the transaction, as well as collateral types.

We limit ABCP issuers to those that are supported by approved bank counterparties. Collateral performance is made available in monthly reports published by each sponsor and our credit team closely monitors the change in collateral composition and concentration, credit performance of assets, and transaction-level credit enhancements.

We utilize ABCP in a manner which minimizes issuer concentration risk by focusing on diversification. This includes aggregating ABCP holdings with holdings from bank(s) that provide credit and liquidity support when evaluating issuer diversification limits. This is a more conservative approach than some peer investment managers. We believe this is consistent with our view that having a lower allocation to a broader array of names is consistent with prudent risk management practices and limits the adverse impact that any one issuer can have on a portfolio.

Lastly, we always emphasize the importance of liquidity within a client’s portfolio. For our separately managed account (SMA) portfolios, this means having allocations to sectors such as Treasuries and Federal Agencies, which are typically the most liquid instruments in the short-term fixed income markets. In our LGIP portfolios, this means managing our liquid pools in accordance with Government Accounting Standards Board 79 (GASB 79) which requires a minimum amount of daily and weekly liquidity at all times.3 These approaches allow us to not be overly reliant on credit markets for the first line of liquidity in our portfolios.

When managed correctly, we believe ABCP can be a diversifier in portfolios that can safely add yield relative to other short-duration investments.

Sources

[1] https://www.federalreserve.gov/releases/cp/.

[3] “Summary of Statement No. 79.” Government Accounting Standards Board. https://gasb.org/page/pronouncement?pageId=/standards-and-guidance/pronouncements/summary-statement-no-79.html&isStaticPage=true.