Why Maintaining an Exposure to International Equities Makes Sense

June XX, 2025

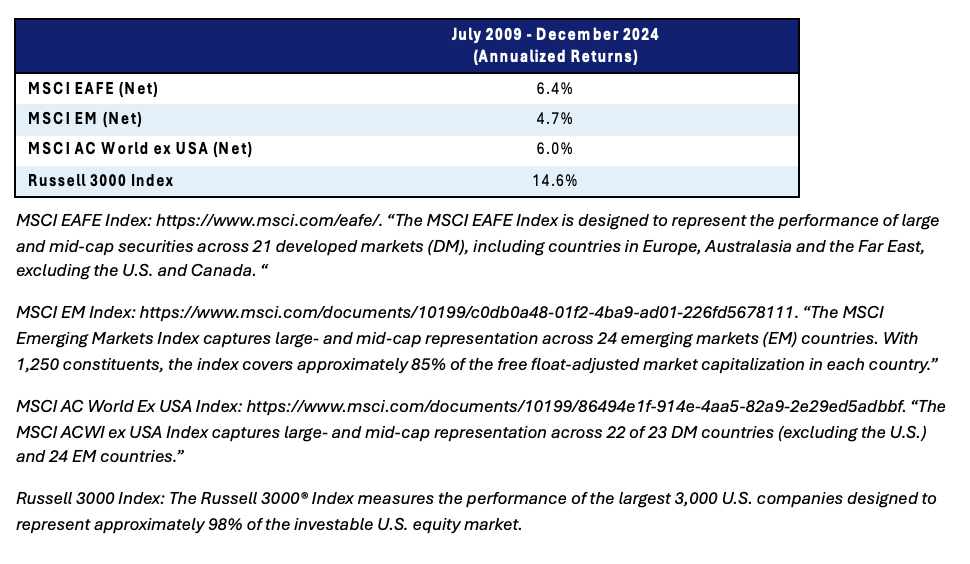

Domestic equities have outperformed international equities for more than a decade. This has led some investors to ponder if an allocation to international equities still makes sense within a multi-asset class portfolio. We believe that international equity exposure in a diversified portfolio remains an important portfolio construction building block.

Background in detail

Data clearly shows that international equity returns, which are comprised of market returns across developed and emerging market equities have been anemic when compared to U.S. equity returns since the global financial crisis (GFC). These returns have led some institutional investors to question the merits of maintaining International Equities as part of their strategic asset allocation.

U.S. equities have significantly outperformed international equities since the GFC primarily due to higher profit margins and more consistent earnings growth across U.S. companies, and a heavier tilt to growth stocks in domestic indices, which have outperformed more value-oriented stocks over the last decade.

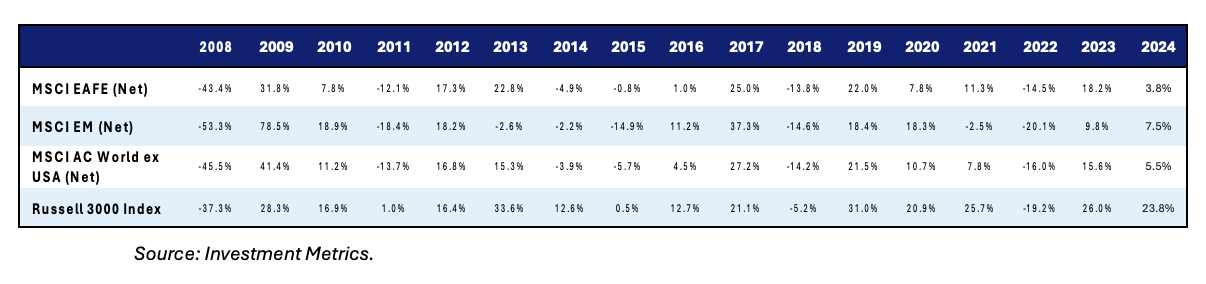

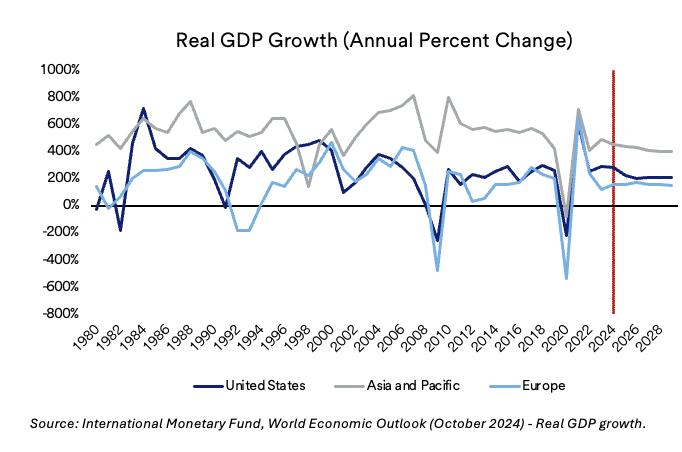

However, this hasn’t always been the case. In the first decade of 2000, there were several periods where international equities outperformed domestic equities. From the start of 2001 until October of 2007, international equities outperformed during a majority of this time period. Domestic equity markets outperformed in several months, but international equities had another run of outperformance from late 2008 until mid-2009. This period of outperformance coincides with the S&P 500 trading relatively flat from 2000-2009, starting with the technology bubble bursting and ending with the global financial crisis, a time period sometimes referred to as “the lost decade.”

When developing strategic asset allocation targets, we utilize long term return expectations, volatility and correlation expectations as part of our portfolio construction process. In our view, the inclusion of an asset class in a multi-asset class portfolio should not be based solely on absolute return expectations, but should also include key drivers of returns, risk and correlations between asset classes. By focusing solely upon absolute return differences over the short- to intermediate-term, investors fail to build a durable, long-term diversified portfolio.

Why has there been such a divergence between U.S. and International Equity returns for the past 20 years?

Actions taken during the Global Financial Crisis

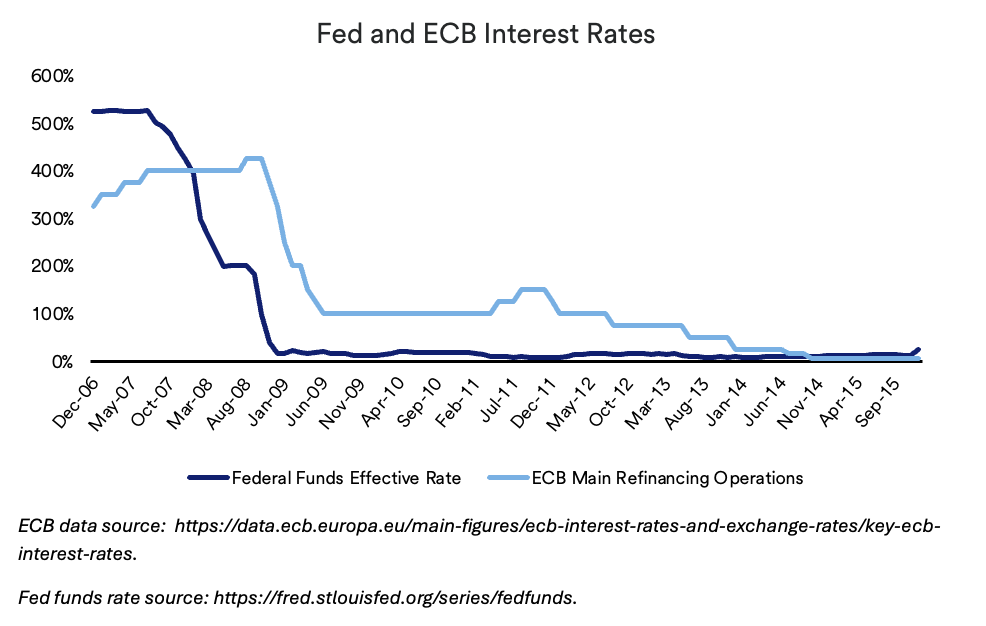

During the GFC, the United States acted quickly to mitigate the housing and banking crisis through the creation of various programs, including TALF (Term Asset-Backed Securities Loan Facility) and TARP (Troubled Assets Relief Program.) The Federal Reserve (Fed) also lowered interest rates aggressively, which served a dual purpose, to stimulate loan growth and to provide a much-needed shock absorber for capital markets. The Fed also aggressively purchased Treasury bonds and mortgage-backed securities (MBS) through its quantitative easing strategy which injected much needed liquidity into the banking system. Finally, companies were allowed to consolidate relatively quickly instead of failing which cleared the excesses that had created an over-leveraged economy. Though a painful time in our economy’s history, the economic downturn quickly reversed itself compared to the much lengthier and more insidious downturn associated with Great Depression.

However, other countries did not enact similar stimulus measures, or were slower to do so, which caused U.S. based entities to “recover” at a quicker pace. In fact, the EU. recovery was hampered by competing national interests and a lack of consensus on how to address local housing market distress. A later sovereign debt crisis which originated in Greece in 2009 before spreading to other nations slowed the recovery process even further.

Even after the global financial crisis was well in the rear-view mirror, the Federal Reserve kept interest rates low for an extended period, which supported valuations in many higher risk, long duration asset classes such as equities, real estate, and private equity. At the operational level, reducing borrowing costs for corporations and businesses also helped to boost earnings.

Post GFC, the profit margins for U.S. companies improved relatively quickly and returned to their pre-GFC high by 2016. Meanwhile, international equities continued to struggle with slower profit margin recovery as economic growth remained anemic particularly across Europe due to an ongoing sovereign debt crisis. International equities, as represented by MSCI ACWI ex USA benchmark returned to their pre-GFC profit margin levels in 2021.

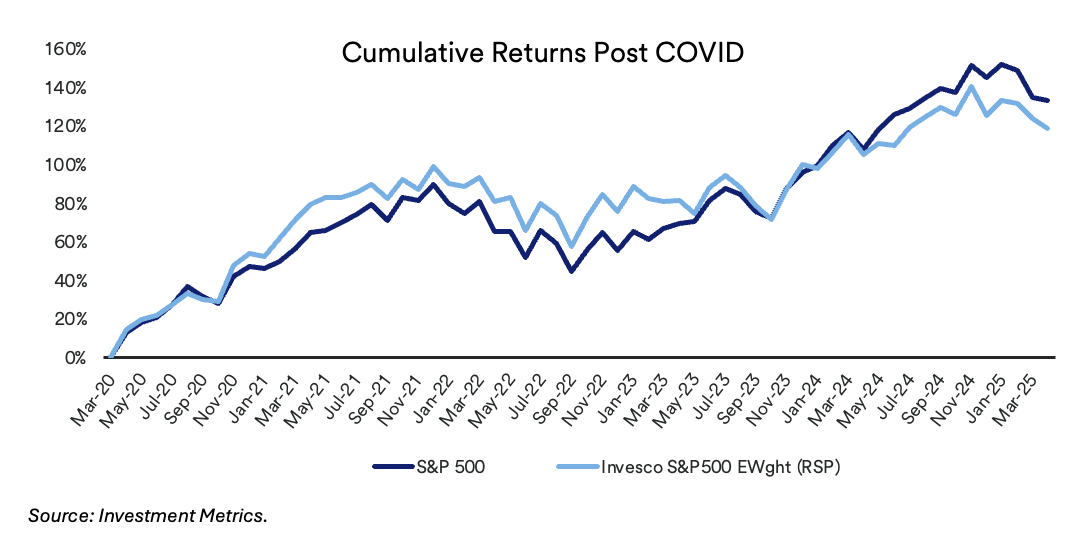

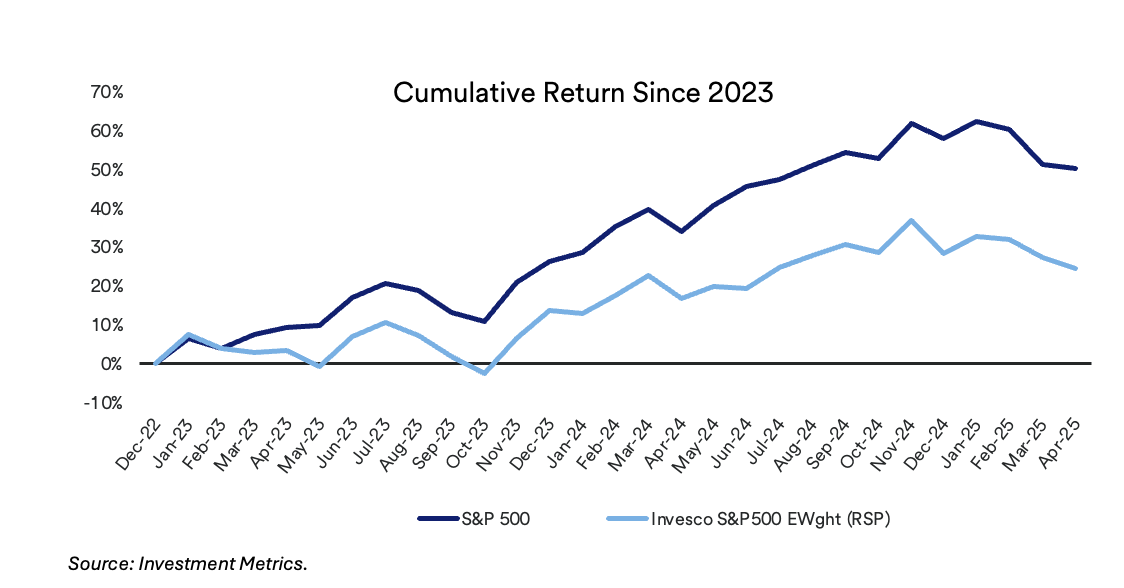

Post COVID, the Magnificent Seven Phenomenon Have Been a Major Driver

The Magnificent Seven (Apple, Tesla, Microsoft, Amazon, Google, Meta, and Nvidia) have pulled equity markets higher in the post-COVID time frame despite the recent hiccups during the first quarter of 2025. The table below highlights the returns and how these stocks have outgained both domestic and international markets, but even more importantly when comparing the market weighted S&P 500 index to an equal weighted S&P 500 index, we see how much these companies have disproportionately outperformed the average company.

These stocks have benefitted from several trends including the growing demand from artificial intelligence (AI) and the fact that each of these companies is classified as a “growth stock” (earnings growth higher than gross domestic product (GDP) and average market earnings growth).

Reasons We Believe International Equities Remain a Critical Strategic Asset Class

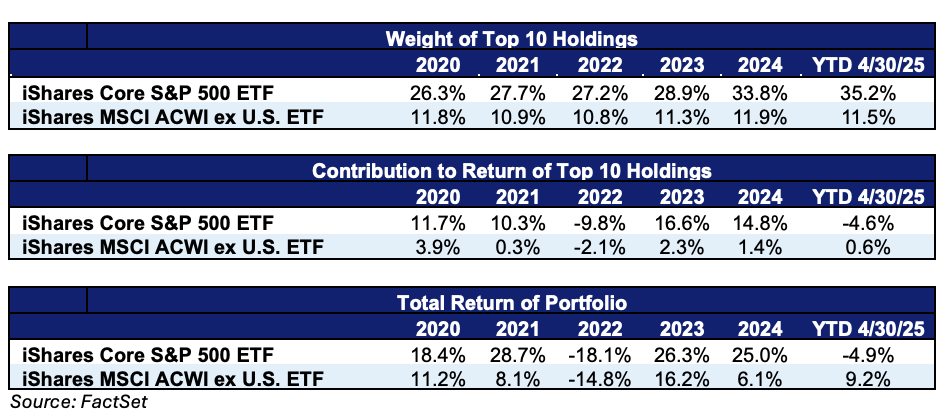

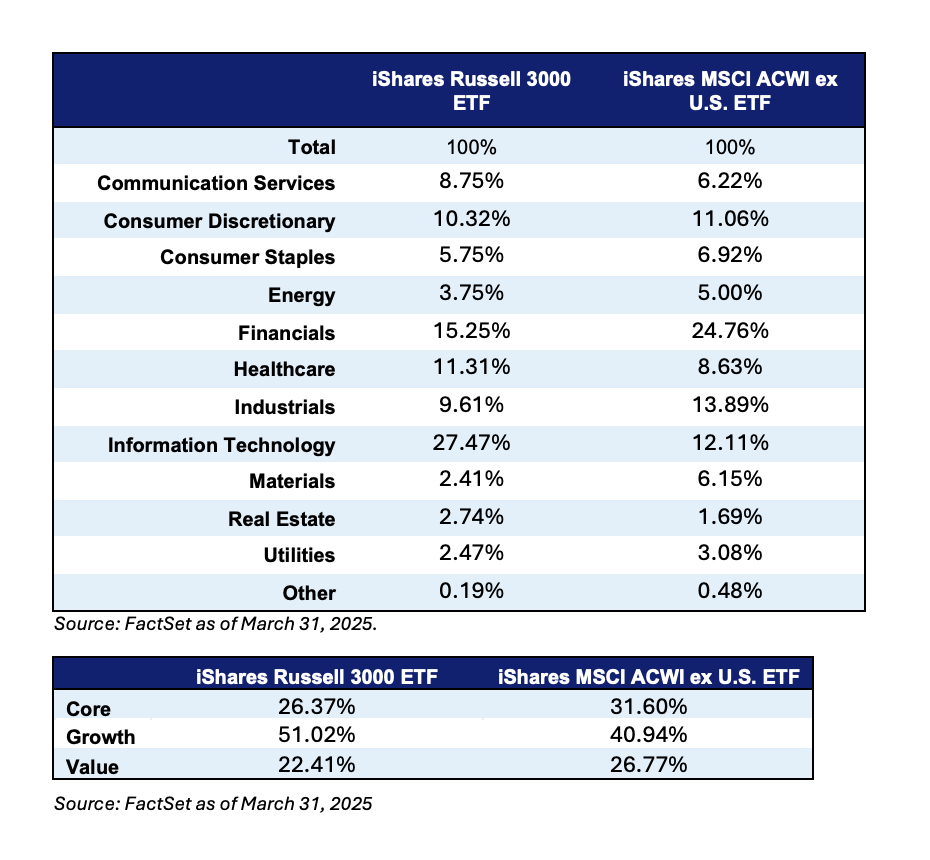

Industry and regional economic diversification: From a sector perspective, the major U.S. equity indices are dominated by technology stocks. In fact, technology issues, which have fared particularly well over the last 15 years, constitute about 40% of the S&P 500 and 33% of the Russell 3000. Meanwhile, the major international equity indices provide greater exposure to other sectors which represent significant parts of the global economy and trade at much lower valuations than technology stocks. In fact, two of the major international indices are dominated by Financials (approximately 23% for MSCI EAFE and 24% for MSCI ACWI ex-U.S.) and Industrials (18% for MSCI EAFE, 14% for MSCI ACWI ex-U.S.) Also, when it comes to geographical exposure, these international equity indices maintain allocations to the United Kingdom, France, Japan, Taiwan, and China, each of which offer unique growth opportunities and regional economic diversification.

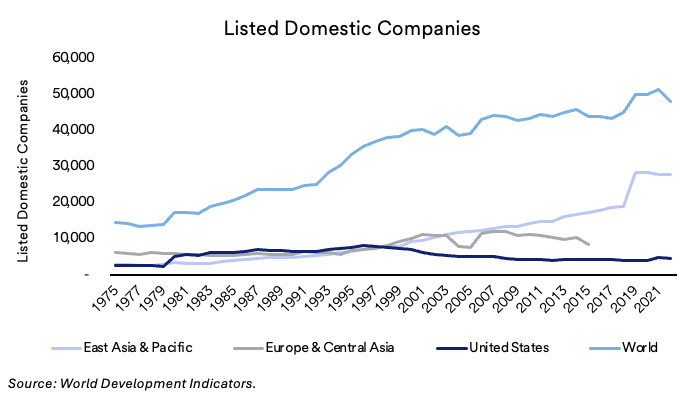

Another advantage of investing internationally is the potential access it provides newly formed public companies. U.S. companies have gone through a period of consolidation and as a result, initial public offerings (IPOs) haven’t been particularly robust in recent years. Also, at least anecdotally, some companies seem to be staying private for a longer period due to the costs associated with becoming public. This has resulted in fewer public companies in which to invest.

Using the Wilshire 5000, which historically has been considered the index for the total of all publicly listed companies, as an example, in prior years, the index consisted of the top 5000 publicly listed companies, as the name suggests. However, it currently comprises about 3500 companies, which highlights the shrinking pool of public domestic companies. On the other hand, a greater number of international companies, especially within emerging markets are going public as these economies continue to grow at a rapid pace, offering potential opportunities for public market investors. In short, adding international exposure may, in some cases, markedly increase the number of companies that one can invest in.

Finally, international investing also allows for exposure to unique companies and markets that are in different phases of development. By definition, developing nations will include more companies that can build and develop new infrastructure as these countries are in maturing phases of economic development, while developed economies tend to be more dominated by service-based companies. In short, this broader exposure provides additional opportunity for investors.

Put simply, international equities provide greater diversification and exposure to countries, sectors and individual companies that may be overlooked if one were to invest solely in a domestic equity index. Investing internationally also allows for greater access and investment in new public companies. Additionally, imperfect correlations between domestic and international equity markets allow for returns and opportunity to reduce portfolio volatility over time.

Favorable demographic trends and the higher GDP growth potential of an emerging consumer base: Emerging markets are often characterized by rapid wealth growth and consumption from a much lower base. In short, EM-domiciled companies are well-positioned for rapid sales and earnings growth that is unlikely to be replicated in a more mature and wealthy economy such as the U.S.

Domestic and international equities have traded performance leadership positions at various points in time over the last several decades. We are in the midst of an extended period whereby domestic equities have maintained a clear leadership position. However, that is unlikely to continue in perpetuity. Timing the inflection points of these leadership changes is exceptionally difficult, which is why we believe the best portfolio practices include participation in both domestic and international equities at all times.

Should you have any questions about this report, please reach out to your relationship manager.

Sources

Investment Metrics

World Development Indicators

FactSet

International Monetary Fund, World Economic Outlook (October 2024) - Real GDP growth