Quarterly Portfolio Manager Commentary

June 30, 2025

Summary

- The first quarter of 2025 was characterized by uncertainty and worsening consumer sentiment due to the volatile rollout of the new administration’s policies. Pro-growth fiscal policies proposed on the campaign trail including tax cuts and deregulation have yet to be realized, leaving rapidly changing tariff policy to weigh on growth prospects. Escalating trade tensions from tariffs have increased the probability of a U.S. economic recession in 2025.

- Progress towards the Federal Reserve’s (Fed) 2% target remains stalled with goods inflation moving higher even before tariff policies were enacted. Fed Chair Powell noted economic data has not yet reflected tariffs and reiterated it will be difficult to directly project the impact of these policies on prices. Tariff concerns among consumers appear to be rising, as expectations for inflation over the next 12 months reached their highest levels since early 2023.

- The labor market remains surprisingly resilient with both initial jobless claims and the unemployment rate at historically low levels. Additionally, monthly job gains continue to keep pace with labor force growth. With quits and hiring rates low, any acceleration in layoffs may result in job seekers remaining unemployed for longer. Federal job cuts and funding freezes could impact the hiring plans of sectors such as healthcare and higher education which rely on government funding. The impact of immigration policy remains unknown.

- The Fed left the overnight policy rate range unchanged at 4.25% - 4.50%. While the Fed’s updated March “dot plot” continues to suggest 50 basis points (bps) of rate cuts in 2025, Fed Chair Powell indicated there is heightened risk and more uncertainty due to the new administration’s policies.

- Sentiment has meaningfully deteriorated as consumers expect higher prices and weaker labor market conditions as tariffs weigh on the pace of economic growth.

- A material deterioration of labor market conditions remains the biggest risk factor to consumer spending. Other headwinds include slower real wage growth and a reduced willingness and ability to spend as prices move higher due to tariffs.

Economic Snapshot

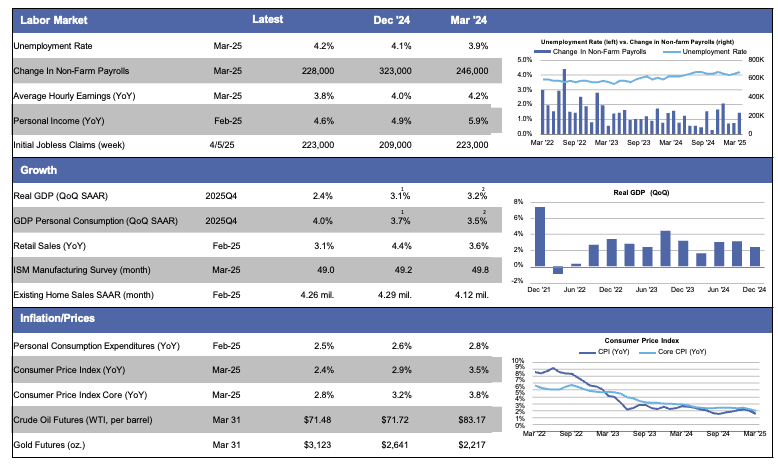

- U.S. inflation readings remained ‘sticky’ during Q1 and did not show meaningful progress towards the Fed’s 2% target. Goods inflation, which had been a detractor from inflation, increased at the beginning of the year and will continue to be a headwind given the expected impact of tariffs on goods prices. Core CPI, which excludes the volatile food and energy components, remained above 3% and ended the quarter at 3.1% annualized YoY while headline CPI sits at 2.8%.

- U.S. real gross domestic product (GDP) remained strong in Q4, with final estimates showing growth of 2.4%. Personal consumption remained strong and grew at the fastest pace in years. The implementation of expansive tariff policy serves as a headwind moving forward, with many Wall Street firms forecasting lower growth and higher inflation for the balance of the year.

Interest Rates

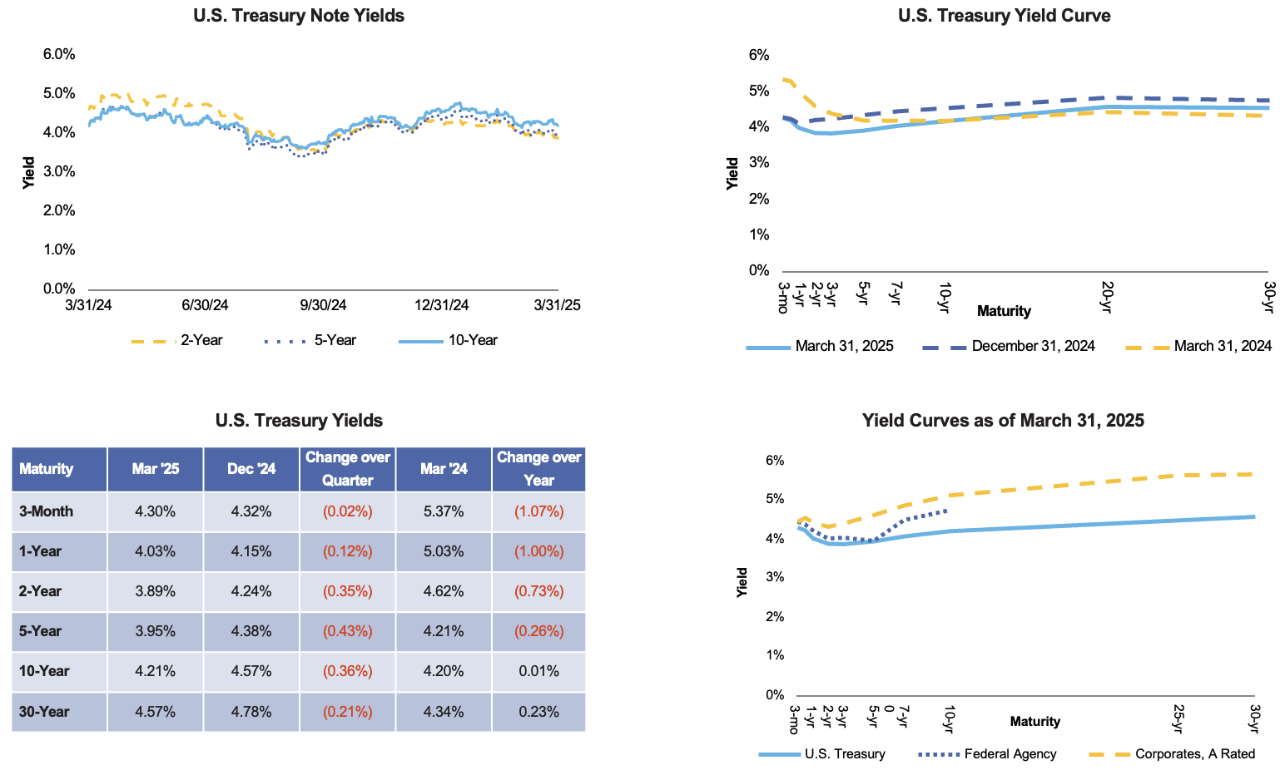

- U.S. Treasury yields moved lower in response to deteriorating growth expectations over the near term. While the Fed held rates steady over the quarter, futures markets are pricing in four 25 bps rate cuts for 2025.

- The yield on the 2-, 5-, and 10-year Treasuries ended the quarter at 3.88%, 3.95%, and 4.21%. This represents a decline of 36 bps, 43 bps, and 36 bps, respectively. The 3-month Treasury was relatively unchanged given no rate cuts from the Fed.

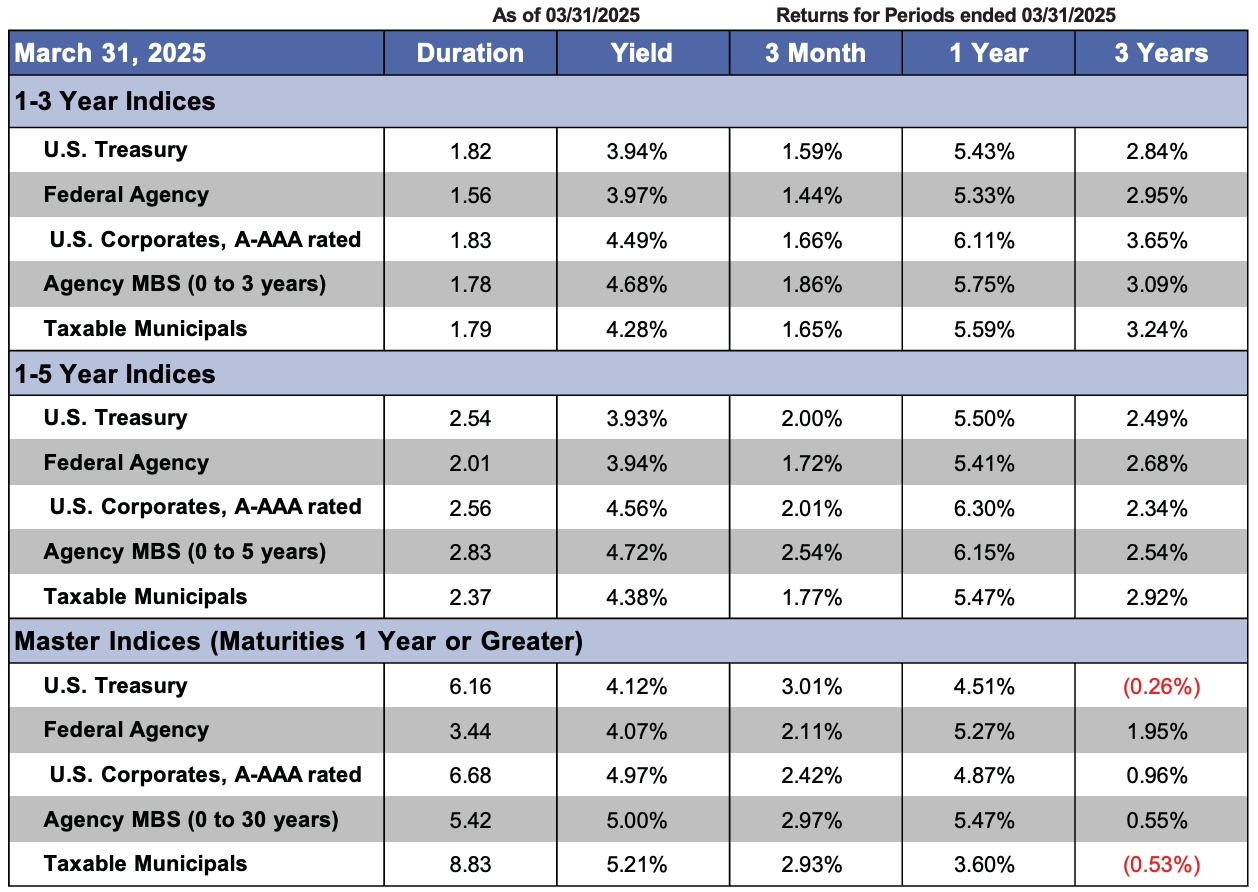

- As a result of lower yields, U.S. Treasury indexes generated positive total returns for the quarter. The ICE BofA 2-, 5-, and 10-year U.S. Treasury indexes returned 1.56%, 2.93%, and 4.01% for the quarter, while the shorter-duration ICE BofA 3-month U.S. Treasury index returned 1.02%.

Sector Performance

- Excess returns were mixed across investment grade sectors as wider economic uncertainty opened the door for modest spread widening off recent lows despite strong investor demand.

- Federal agency & supranational spreads remained low and rangebound throughout Q1. Federal agencies produced modestly negative excess returns while supranationals were slightly positive. Issuance remained light and incremental income from the sectors is near zero.

- Investment-grade (IG) corporate bonds inside 10 years produced positive excess returns as much of the spread widening seen during the second half of the quarter was offset by higher incremental income. Excess returns of financial and banking issuers continued to lead most other industries during the quarter.

- Asset-backed securities (ABS) spreads widened modestly from the impact of heavy new issuance and a moderate deterioration of credit fundamentals. ABS spreads widened more than corporate spreads, resulting in worse performance over the quarter, but better relative value going forward. ABS excess returns were generally negative for the quarter, with credit cards outperforming automobile collateral.

- Mortgage-backed securities (MBS) performance was mixed across structure and coupon during Q1 as heightened rate volatility persisted. Shorter, 15-year collateral MBS posted positive excess returns while longer, 30-year collateral MBS were firmly negative during Q1. Agency-backed commercial MBS (CMBS) saw positive excess returns across collateral and coupon structures.

- Short-term credit (commercial paper and negotiable bank CDs) yields on the front end fell in response to downward pressure from a paydown in the supply of U.S. Treasury Bills. Yield spreads tightened over the quarter in response to moderated issuance and strong demand.

Economic Snapshot

1. Data as of Third Quarter 2024.

2. Data as of Fourth Quarter 2023.

Note: YoY = year-over-year, QoQ = quarter-over-quarter, SAAR = seasonally adjusted annual rate, WTI = West Texas Intermediate crude oil. Source: Bloomberg.

Interest Rate Overview

Source: Bloomberg

ICE BofA Index Returns

Returns for periods greater than one year are annualized.

Source: ICE BofA Indices.

Jim Palmer, CFA